-

Jimmy Jean • Randall Bartlett • Benoit P. Durocher • Royce Mendes • Hélène Bégin • Tiago Figueiredo

Francis Généreux • Lorenzo Tessier-Moreau • Hendrix Vachon

Economic and Financial Outlook

The Last Mile of Disinflation: The Fed Falls Behind

April 25, 2024

Highlights

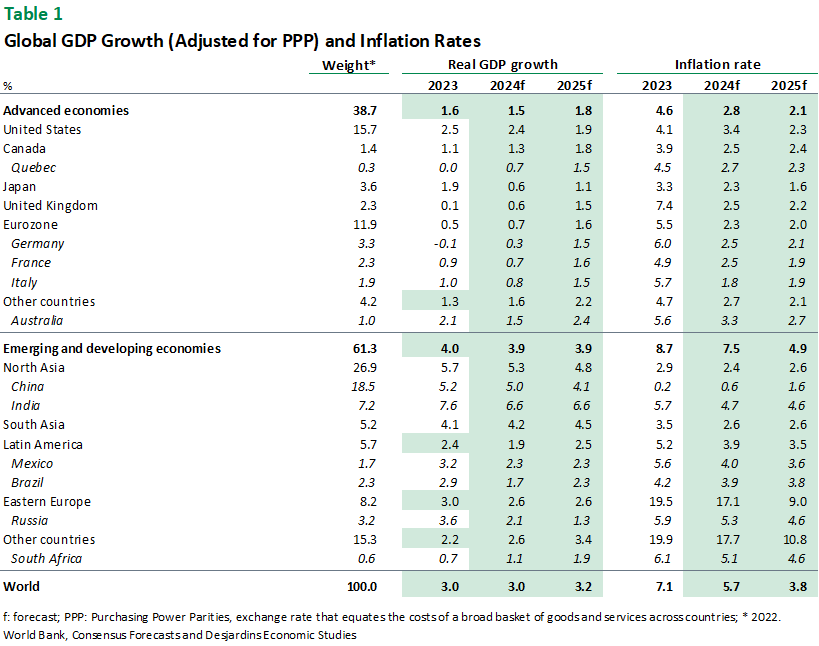

- The global economy is showing signs of improvement despite the fact that geopolitical tensions have led to increased price volatility for stocks and commodities, with oil prices being particularly hard hit. China posted solid real GDP growth in the first quarter of 2024. In the eurozone, PMIs offer better prospects after several quarters of economic stagnation—with the biggest improvement being in the services sector—though we have yet to see signs of substantial improvement. Inflation has continued to trend in the right direction, which means the European Central Bank could soon announce the start of interest rate cuts.

- In the United States, various indicators have underscored the relative strength of the economy. But the resilience of the US economy, and especially its labour market, has translated into more persistent inflation, with services inflation being particularly sticky. Against this backdrop, the Federal Reserve will hold off until the fall before initiating monetary easing.

- Economic data continue to outperform expectations in Canada, with real GDP growth coming in stronger and inflation weaker than anticipated to start 2024. The labour market has also shown tentative signs of a slowdown. If this trend persists through to the Bank of Canada’s next interest rate announcement, it will all but cement our call for rate cuts to begin in June. The Bank should gradually ease monetary policy thereafter, as ongoing mortgage renewals at higher rates continue to squeeze household budgets and weigh on consumption. Our research found that if implemented as stated, the recently announced plan by the federal government to reduce non‑permanent resident admissions will put additional downward pressure on real GDP growth and inflation over the medium‑term. On the fiscal policy front, the new spending measures announced during budget season shouldn’t materially impact the outlook for inflation. But new measures in the federal budget should tip the scales toward greater investment in residential construction and less business investment. (See our analysis of Budget 2024 for more information.)

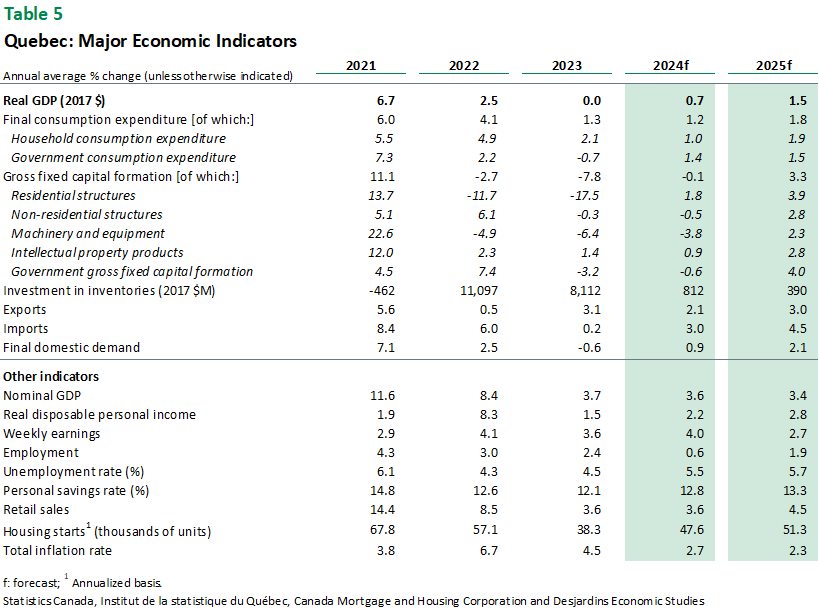

- Meanwhile Quebec has seen some of its economic indicators tumble since last fall's public sector strikes, and the province's real GDP fell for three consecutive quarters from spring 2023 to the end of the year. Real GDP rebounded 1.9% in January thanks in large part to employees returning to work in the education and health care sectors, but this improvement is sure to be temporary. Even though the Quebec economy no longer seems to be contracting, it will continue to struggle until the real recovery begins—probably sometime in the second half of 2024. Until then, the labour market will continue to deteriorate. The unemployment rate, which was 5.0% in March, will rise to roughly 6.0% in the coming months. This is significantly higher than the record low of 3.9% from November 2022.

Risks Inherent in Our Scenarios

Inflation has come down, though it remains above target in most countries and other inflationary shocks aren’t out of the question. The odds of additional interest rate hikes are low, but rates could remain at their current level for longer if progress on inflation stalls. There’s also a great deal of uncertainty surrounding the lagged effect of higher interest rates on economic growth. As mortgages continue to be renewed at higher rates, many Canadian borrowers could feel the squeeze. Higher unemployment could also lead to challenges for the housing market. The US presidential election in November could be an inflection point that adds even more uncertainty. Fiscal deterioration in the United States and elsewhere could prompt credit ratings downgrades and possibly push longer-term interest rates higher. Worsening geopolitical tensions could also spell instability for the global economy, financial markets and commodity prices, particularly in the wake of the recent Israel–Iran confrontation, or if the war in Ukraine intensifies again. From a currency perspective, if the global economy encounters new headwinds, many investors may park their assets in US dollars, sending the greenback soaring. A further widening of interest rate differentials with the United States would have the same effect. Rapidly cheapening currencies would in turn have a destabilizing effect for many economies.

Financial Forecast

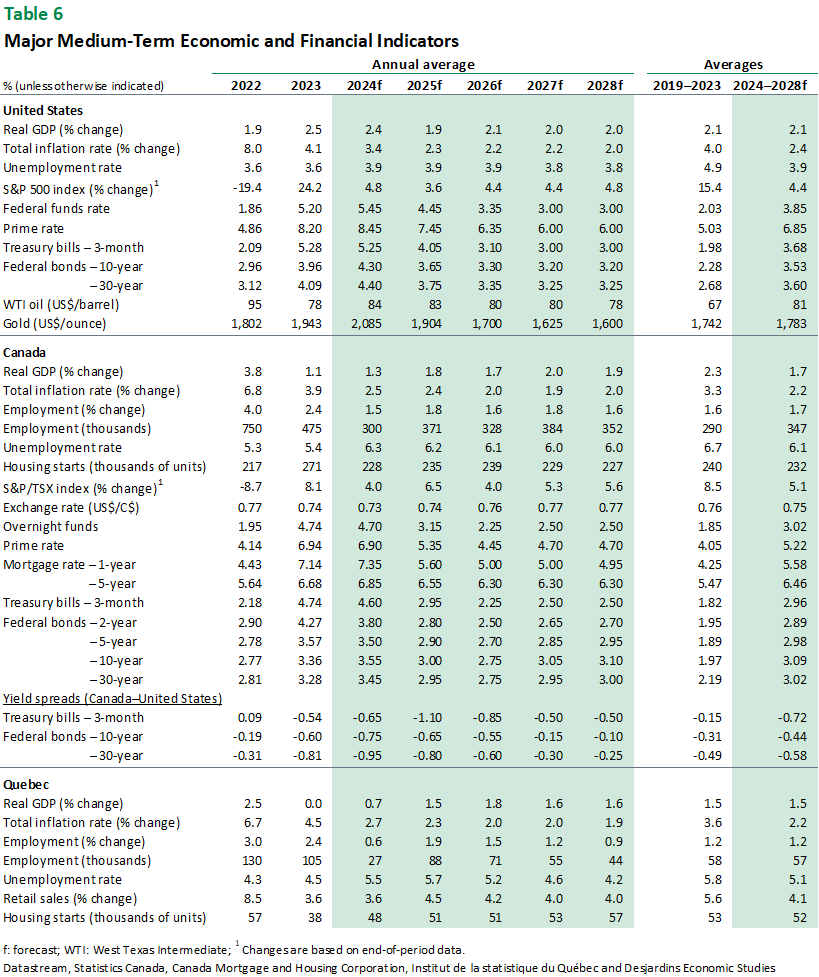

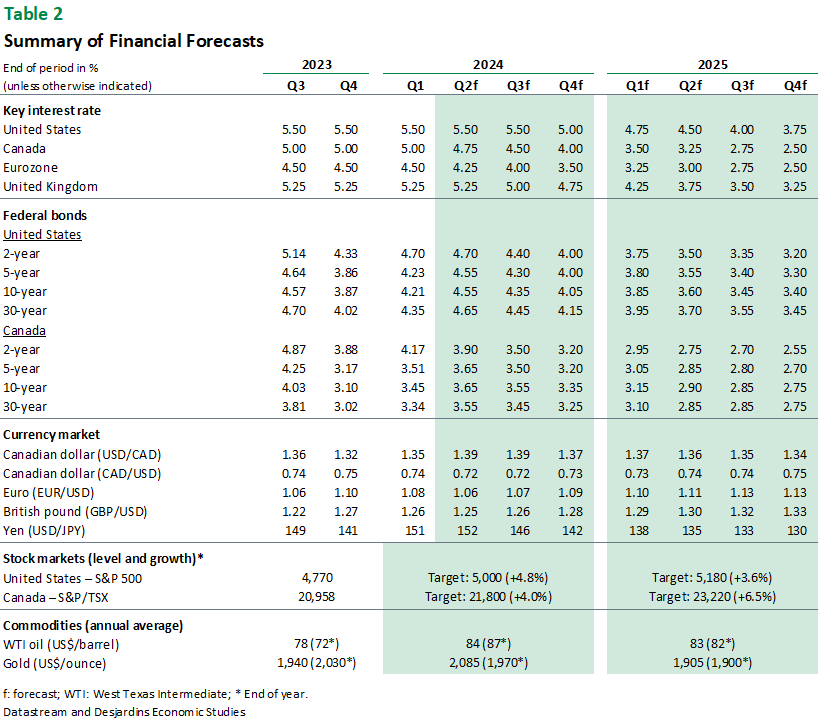

With inflation running persistently high in the United States, many investors now expect interest rate cuts to be more moderate in that country. We've scaled back our forecast to two cuts in 2024. The first should come around fall, provided that inflation eases and the country's economy cools a little. Strong productivity growth in the US should help bring down inflation. On our side of the border, the Bank of Canada may already have enough reason to start cutting interest rates as inflation abates. Canada and the US can take divergent monetary policy paths to a certain extent, but not without impacting the Canadian dollar. The loonie has already depreciated in the past few weeks, as have several other currencies. It will likely remain low for another few months and could even momentarily reach CAN$1.40/US$. Rising bond yields recently dampened the stock market rally, and while several valuations remain high, there's room for them to fall in the coming months.

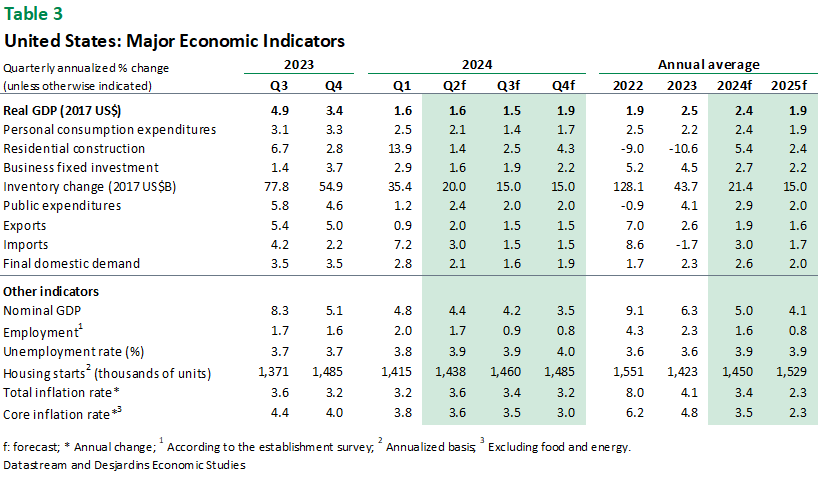

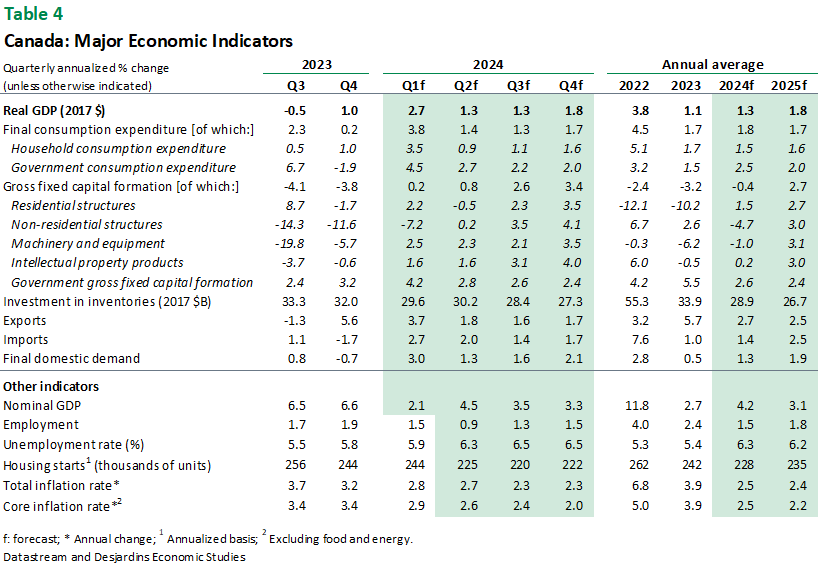

Forecast Tables