- Randall Bartlett

Senior Director of Canadian Economics

Essentials of Monetary Policy

Not Two and through, as the BoC Tees Up More Cuts to Come

July 24, 2024

According to the Bank of Canada (BoC)

- As was widely expected, the Bank of Canada cut the overnight policy rate by 25 basis points for the second consecutive meeting, to 4.50%. That’s the lowest it’s been since May 2023.

- Governor Macklem struck a dovish tone in his press conference opening statement, citing three key considerations that underpinned the decision. “First, monetary policy is working to ease broad price pressures.” Second, excess supply in the economy and slack in the labour market mean “the economy has more room to grow without creating inflation pressures.” Third, and maybe most importantly, as inflation gets closer to 2%, the risk that price growth comes in lower-than-expected increases.

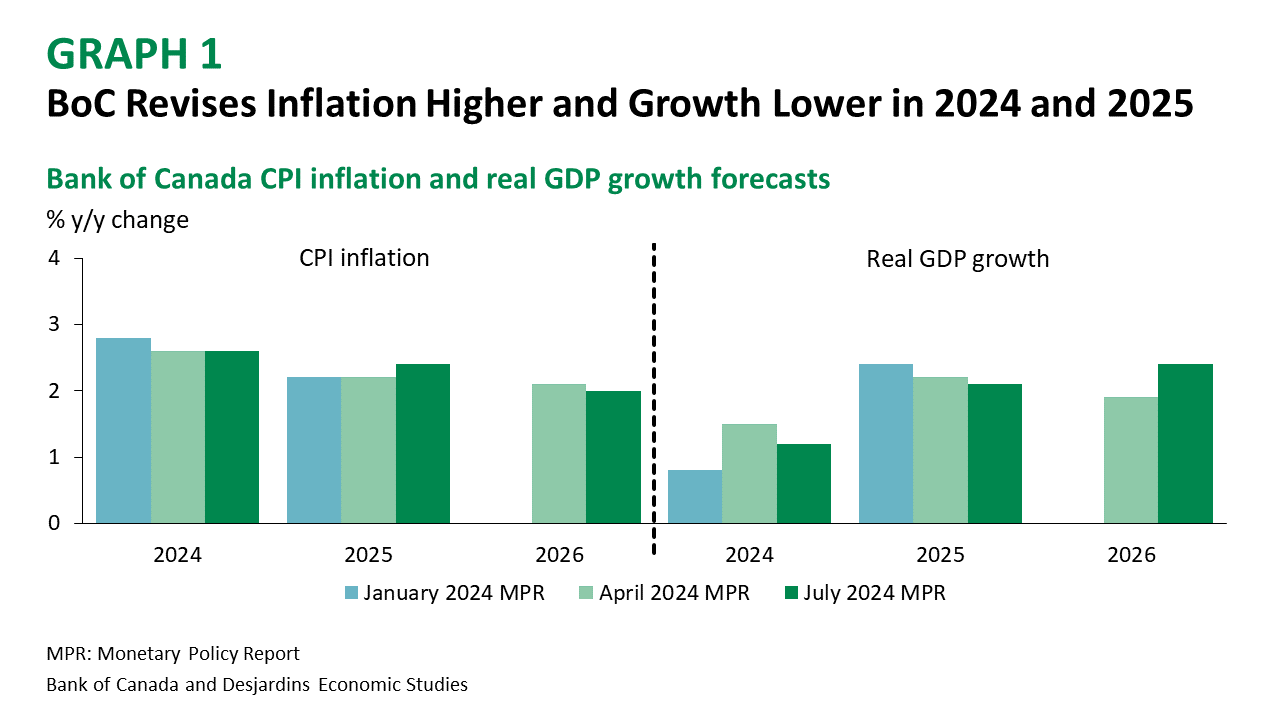

- In this context, the Bank had to adjust its outlook for CPI inflation as it was weaker than the Bank had expected in Q2 2024, averaging 2.7% versus the Bank’s prior forecast of 2.9% for Q2. However, the Bank still expects inflation to average 2.6% for all of 2024, as it ends the year at a more elevated 2.4% (the prior forecast was 2.2%). That handoff sets up 2025 for higher inflation than previously expected (graph 1), revised up to 2.4% from 2.2% in the April Monetary Policy Report (MPR). In contrast, the inflation outlook is a tick lower in 2026 than it was previously, now at 2.0%.

- Meanwhile, it was inevitable that the Bank was going to have to revise down its real GDP growth forecast for 2024 (to 1.2% from 1.5%), as the data have been coming in below its April expectations (graph 2). This despite a very optimistic outlook for Q3 real GDP growth of 2.8%, which is well above our current tracking. In 2025, growth was also revised down to 2.1% from 2.2% in the April 2024 MPR. In contrast, real GDP growth in 2026 was revised up substantially, by 0.5 percentage points to 2.4%. This upward revision can be almost entirely explained by a rosier outlook for population growth in the year, in contrast to the latest demographic projections published by Statistics Canada. We believe this points to downside risk to the Bank’s outer year forecast.

- Looking ahead, Governing Council sees “broad price pressures continuing to ease” and expects “inflation to move closer to 2%” as “ongoing excess supply is lowering inflationary pressures.”

- The Bank of Canada also recommitted to its policy of balance sheet normalization. As a result, the central bank will continue quantitative tightening, allowing bonds to mature and roll off of its balance sheet, thereby reducing its footprint in the Government of Canada bond market.

Implications

Another rate announcement, another rate cut. And while Governing Council didn’t provide any explicit guidance about what comes next, there’s a strong sense that policymakers feel an urgency to continue to the rate cutting cycle in September. The dovish language in the releases paints a picture of officials who are growing more worried about the likelihood of recession. As a result, we are pulling forward our rate cut expectations to forecast another move in September. We now expect the Bank of Canada to reduce rates in September and then again in October before pausing in December to assess how lower rates are impacting the economy and inflation.

2024 Schedule of Central Bank Meetings