- Francis Généreux

Principal Economist

Economic News

US Real GDP Growth Eases Up Slightly

April 25, 2024

Highlights

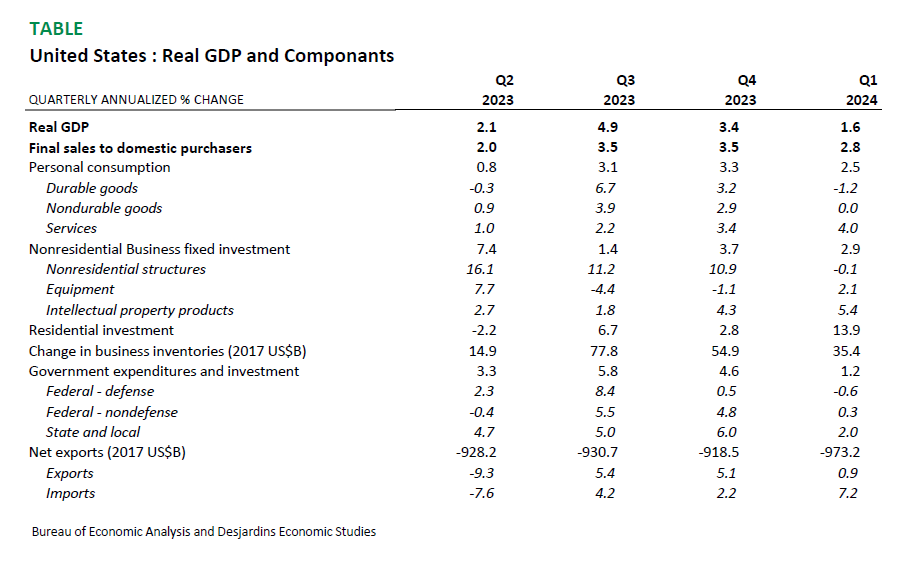

- According to the advance estimate released by the U.S. Bureau of Economic Analysis, real GDP increased at an annualized rate of 1.6% in the first quarter of 2024. This comes on the heels of gains of 3.4% in the fourth quarter and 4.9% in the third quarter of 2023.

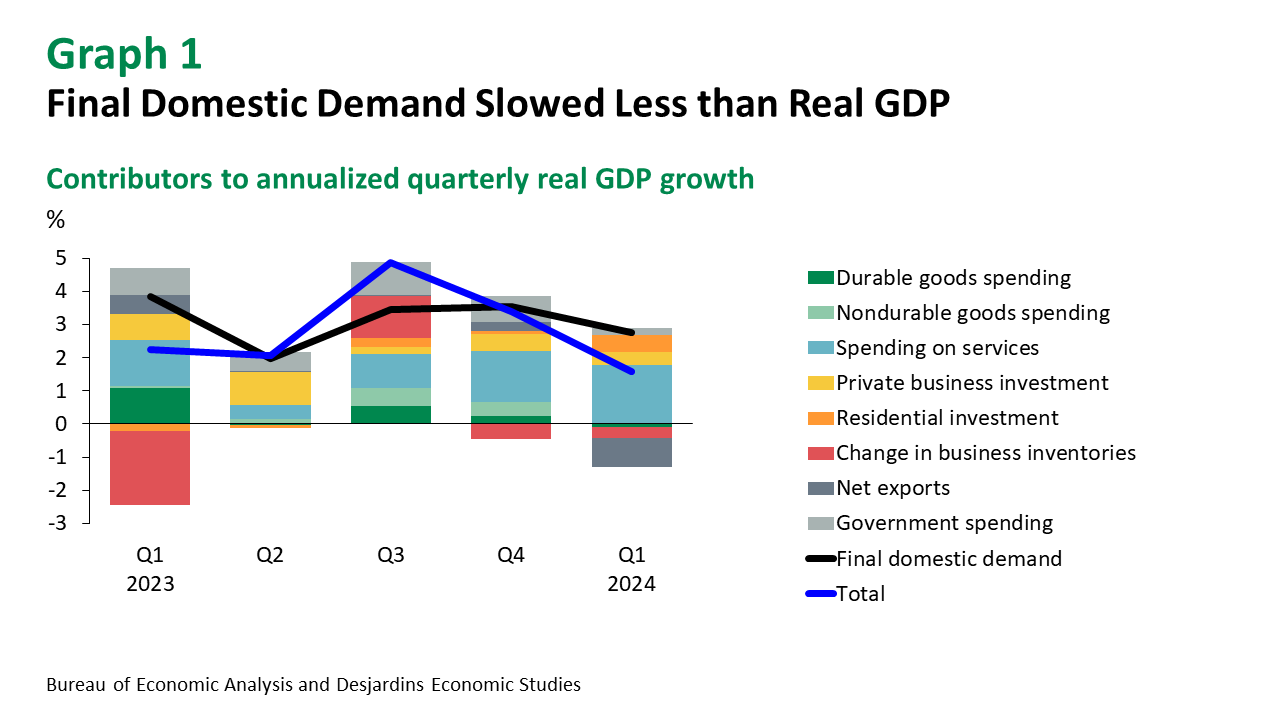

- Meanwhile, final domestic demand picked up, growing at an annualized rate of 2.8% in the first quarter. Net exports and the change in private inventories dragged down real GDP growth.

Comments

After real GDP growth beat expectations by a wide margin in the second half of last year, the 1.6% gain revealed today shows the US economy is growing at a more normal pace that better reflects the high interest rate environment. The uptick also came in below the consensus forecast of 2.4%, and is the weakest quarterly growth since the declines experienced in early 2022.

That said, the US economy is still doing well. In fact, final domestic demand grew by an annualized 2.8%, which isn't exactly a sign of a struggling economy. The pickup in real personal spending on services is particularly noteworthy. It advanced 4.0%, its best quarterly performance since the summer of 2021. This helped offset some softness in durable and nondurable goods (-1.2% and 0%, respectively). Real business investment also ramped up, especially in equipment and intellectual property products. In addition, residential investment jumped 13.9%, the sharpest rise since the end of 2020. However, government spending has slowed.

Strong domestic demand also buoyed real imports, which posted their biggest annualized gain in two years (7.2%). This is in sharp contrast to the modest 0.9% growth in real exports. To meet domestic demand, businesses also accumulated less inventory. The fluctuations in net exports and inventories shaved 1.21 percentage points off real GDP growth. This explains the difference between the upsurge in final domestic demand and weaker real GDP growth.

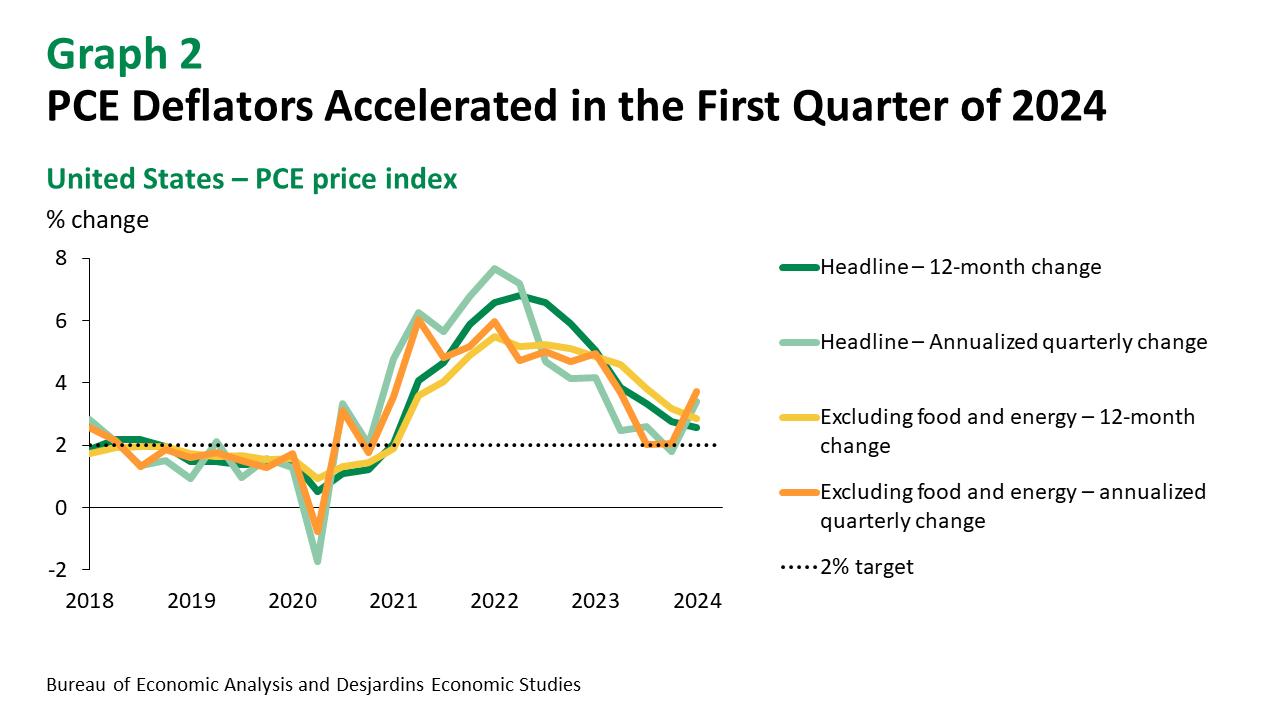

It's also interesting to note that total PCE inflation stayed on a downtrend, slipping from 2.8% in the fourth quarter of 2023 to 2.6% in the first quarter of 2024. But hidden behind the decline is faster annualized quarterly growth, with the total PCE deflator climbing from 1.8% to 3.4% and the core deflator, which strips out food and energy, rising from 2% to 3.7%. This acceleration, which can already be seen in CPI data, will probably convince the Fed to wait several months before it starts cutting rates.

Implications

US real GDP growth has slowed from the second half of 2023. But the US economy is still growing fast enough to drive up prices. The Fed will therefore have to wait longer for evidence that internal inflationary pressures are easing enough to justify rate cuts.