- Francis Généreux

Principal Economist

Economic News

United States: Retail Sales Posted Solid Gains in March, but Not across All Sectors

April 15, 2024

Highlights

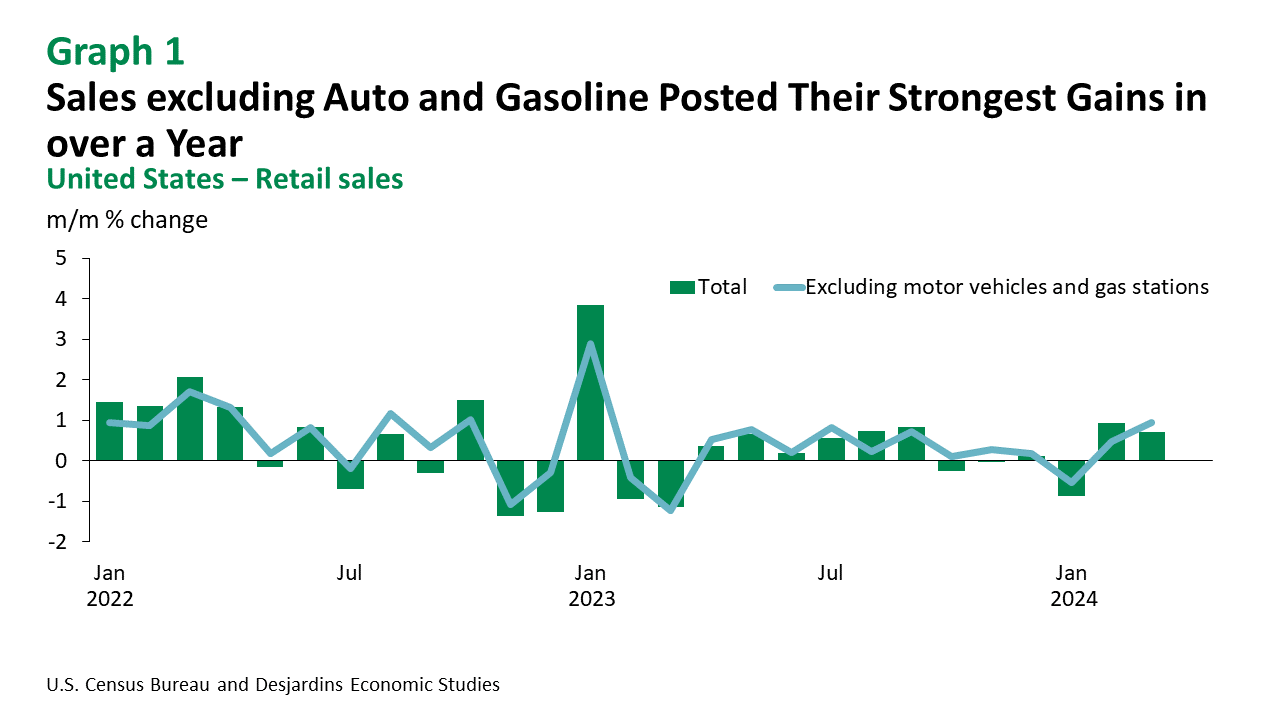

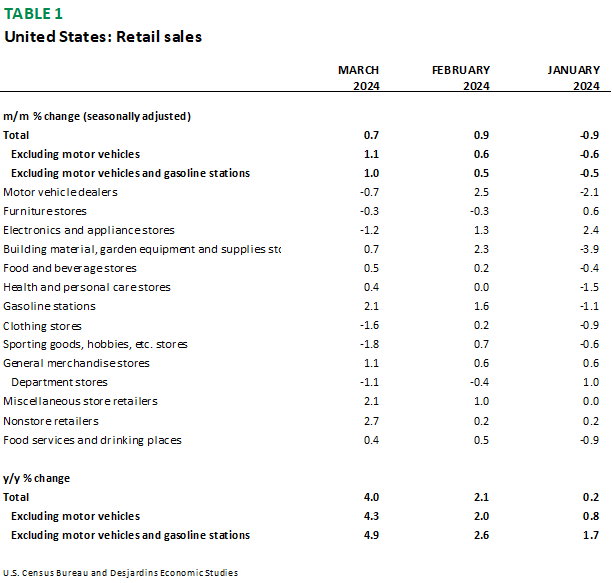

- Retail sales rose 0.7% in March, after gains of 0.9% in February (revised up from 0.6%). Excluding cars and fuel, sales were up 1.0%.

Comments

Retail sales continued to recover in March. The rebound began in February, after a 0.9% drop in January. If we exclude autos and gasoline stations, sales have even begun to accelerate: the 1% increase is the strongest we've seen since January 2023.

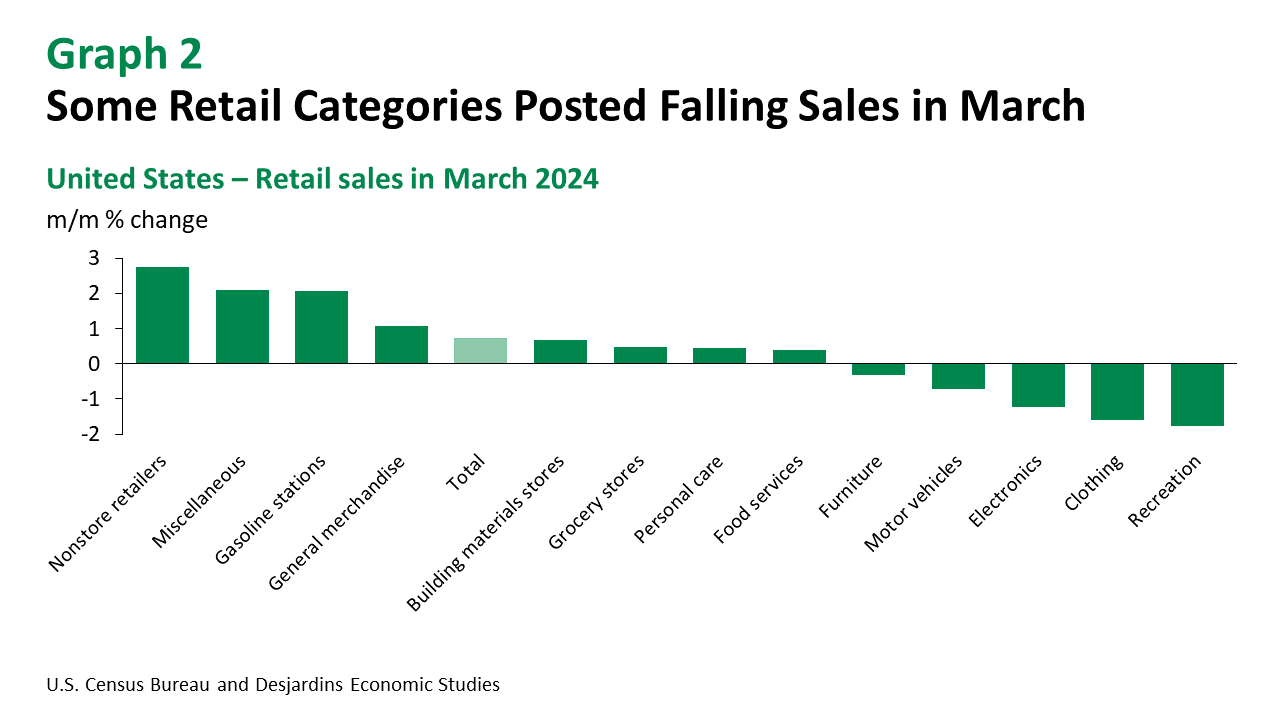

That being said, not all retailers posted gains in March. Sales by motor vehicle and parts dealers slid 0.7%, which is no surprise given the new motor vehicle sales figures that were released at the start of the month. Durable goods sales were also rather weak, particularly for furniture (-0.3%), and electronics and appliances (-1.2%). These results undoubtedly reflect the continued high interest rates. We also noticed poor showings from clothing stores (-1.6%), recreational goods stores (-1.8%) and department stores (-1.1%). All of these declines show that sales growth in March was not very widespread.

So who did come out ahead? Nonstore retailers had the strongest gains, surging 2.7% This is their best monthly growth since January 2022. Without this sector, retail sales would only have grown 0.3%. Other sectors that did well include building materials stores, grocery stores, general merchandise stores (other than department stores), food services and retailers in the "miscellaneous" category.

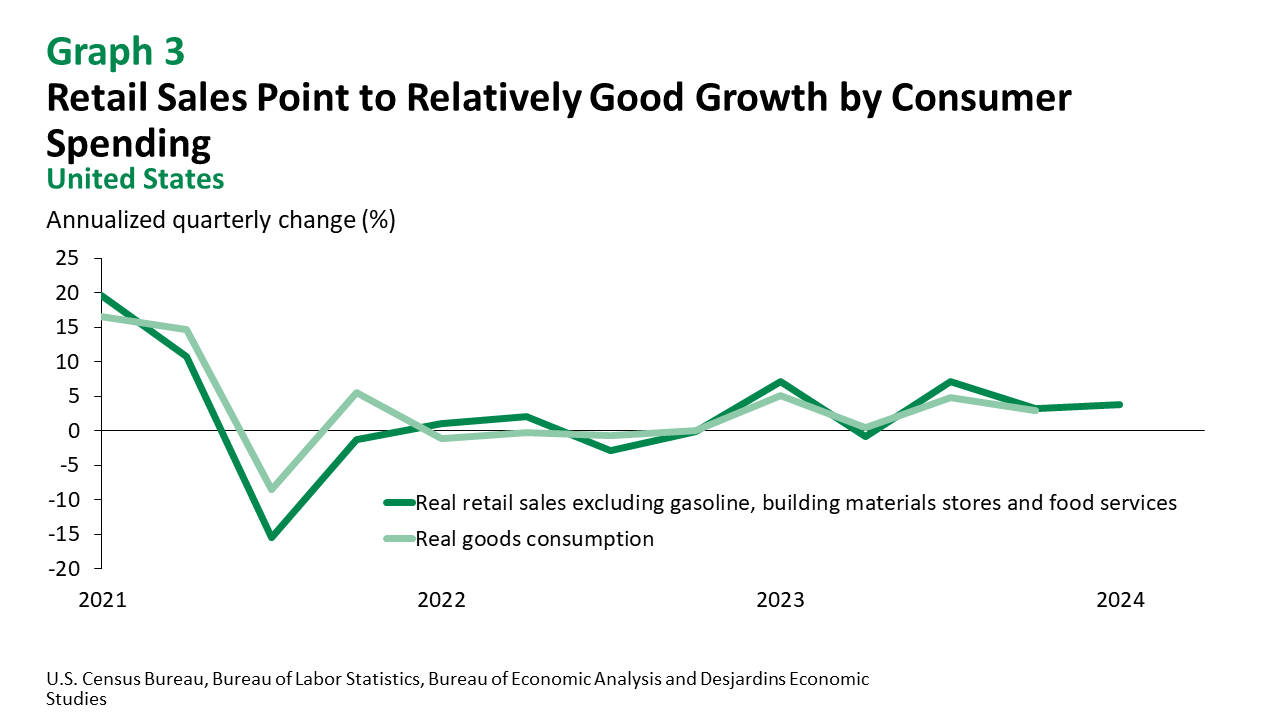

The strong retail sales figures for February and March suggest that real consumption was on the rise in Q1 2024, especially since goods prices have grown at a much weaker pace. While January's data was not good, the situation has changed and household spending could contribute positively to real GDP growth.

Implications

Household spending continues to grow in the United States. Some sectors are experiencing more difficulties than others, but overall sales are doing well despite continued high interest rates. This news, combined with other recent indicators, suggests that the Federal Reserve may be more patient than recently expected when it comes to cutting interest rates.