-

Francis Généreux

Principal Economist

Economic News

United States: Hiring Recovers Slightly, but Remains Disappointing

September 6, 2024

Highlights

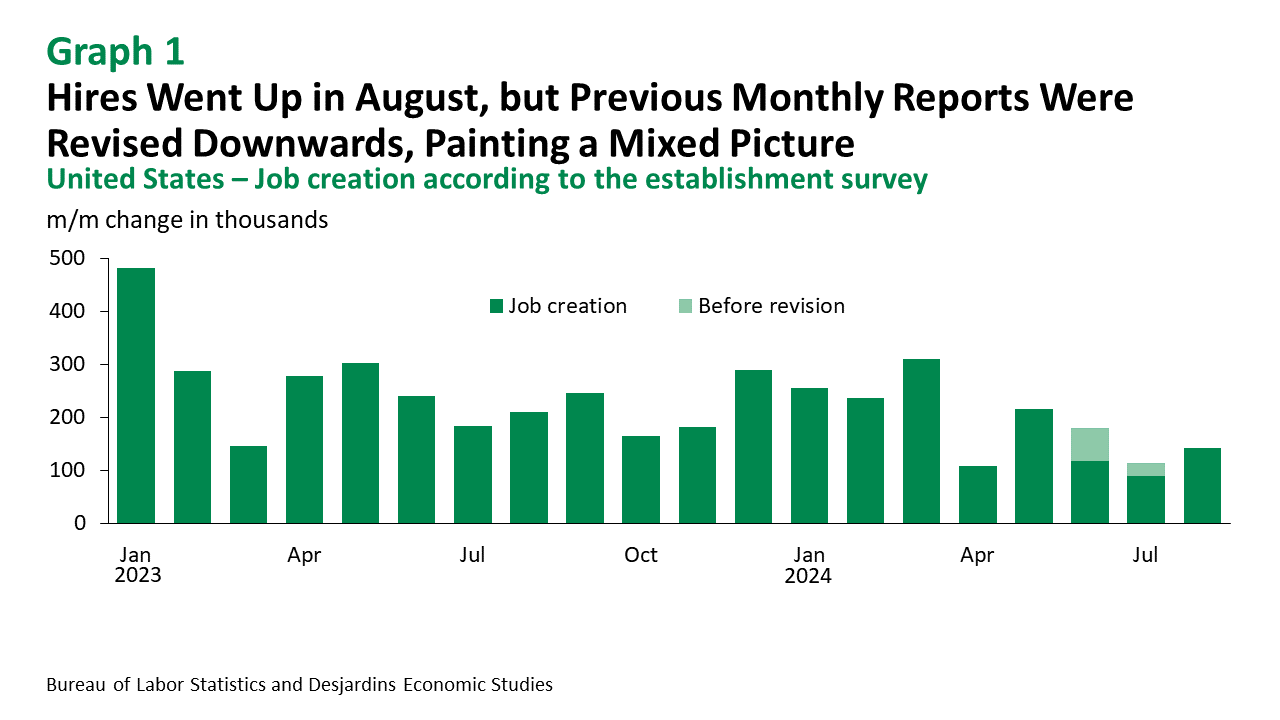

- According to the establishment survey, total nonfarm payroll employment went up 142,000 in August.

- Average hourly wage growth accelerated, with a 0.4% gain in August after July's 0.2% increase. Year-over-year change is 3.8%, versus 3.6% the month before.

- The household survey showed slightly more robust growth, with 168,000 jobs added. The unemployment rate fell for the first time since March, dropping from 4.3% to 4.2%.

Comments

August's labour market results aren't as disappointing as July's, but they still leave much to be desired. The consensus forecast had called for a stronger rebound in net hires (around 160,000 new workers). And the job reports for the last two months were also revised downwards, with July's net job creation falling from 114,000 to 89,000 and June's going from 179,000 to 118,000.

There were hopes—ultimately dashed—that Hurricane Beryl had made a larger contribution to July's weaker numbers, and that we'd see a sharper recovery in August. We can see that worker absences due to bad weather settled down in August after surging in July. Weekly hours did increase, but the return to normal did not give much of a boost to hires over the month. All the same, we can see that of the 250 industries covered by the survey, the proportion where employment increased rose from 47.8% in July to 53.2% in August. That's a clear improvement, but still below the 55.4% average recorded for the first half of 2024. What's more, manufacturing employment appears to have faltered, with durable goods manufacturing shedding 25,000 jobs, including 5,900 in the motor vehicle and parts industry. The 11,000 jobs lost in retail trade are also discouraging. That being said, we should take August's numbers with a grain of salt. We've noticed that August's preliminary employment results tend to come in rather weak, only to be revised upward substantially in future estimates. That has been the case in 11 out of the last 14 years. Hopefully it happens again this year.

The household survey results are painting more optimistic picture of the month than those of the establishment survey—a rare occurrence over the last year. July's unemployment figures had attracted a lot of attention, fuelling fears of an imminent recession. The 168,000 jobs created according to the household survey suggest that unemployment is on the wane, easing some of those fears. In July, the number of unemployed workers was inflated by temporary layoffs; that number went down in August. That said, the situation isn't ideal, and the underemployment rate (which also includes some unemployed discouraged workers and workers who are involuntarily part-time) continued to increase in August. So there is some lingering weakness.

Implications

Even though new hires were up in August, the US labour market still shows signs of slowing. It doesn't yet seem like the US is on the brink of a recession, but the Federal Reserve may be spurred into action. Fed officials are likely hesitating between lowering key rates by 25 or 50 basis points. For the time being, and given the current electoral context, a 25-point cut seems more probable.