- Francis Généreux

Principal Economist

Economic News

United States: Real consumer spending goes down as price indexes go up

February 29, 2024

Highlights

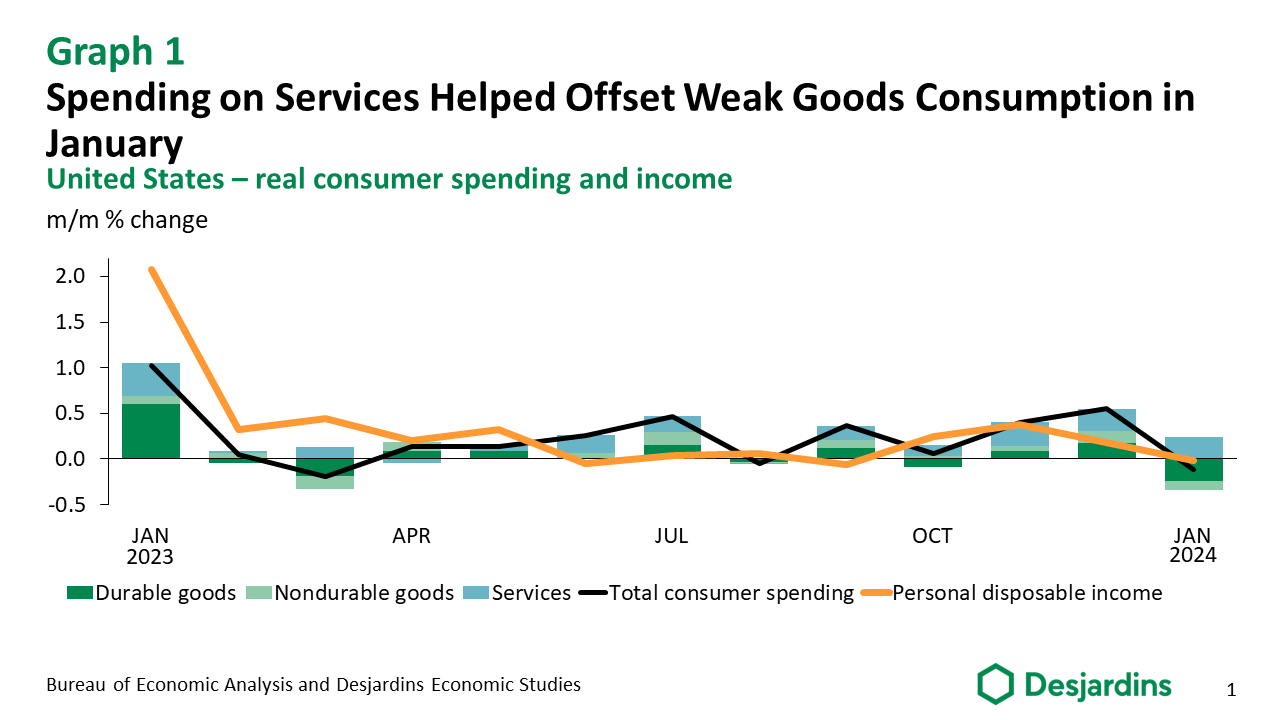

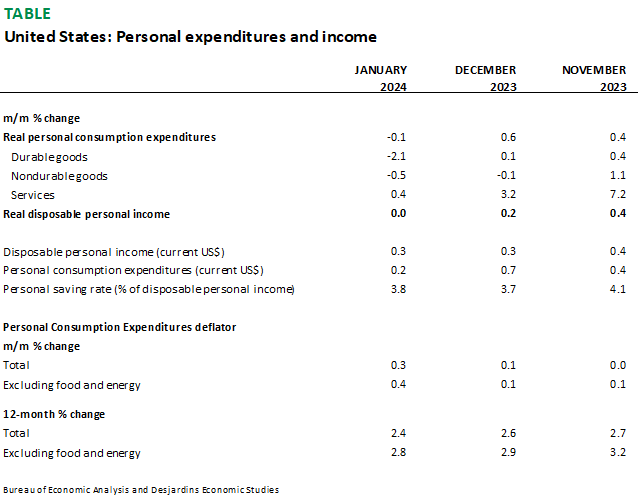

- US real consumer spending fell 0.1% in January after posting solid growth of 0.6% in December.

- Real disposable income stayed flat (0.0%) in January after a 0.2% gain in December.

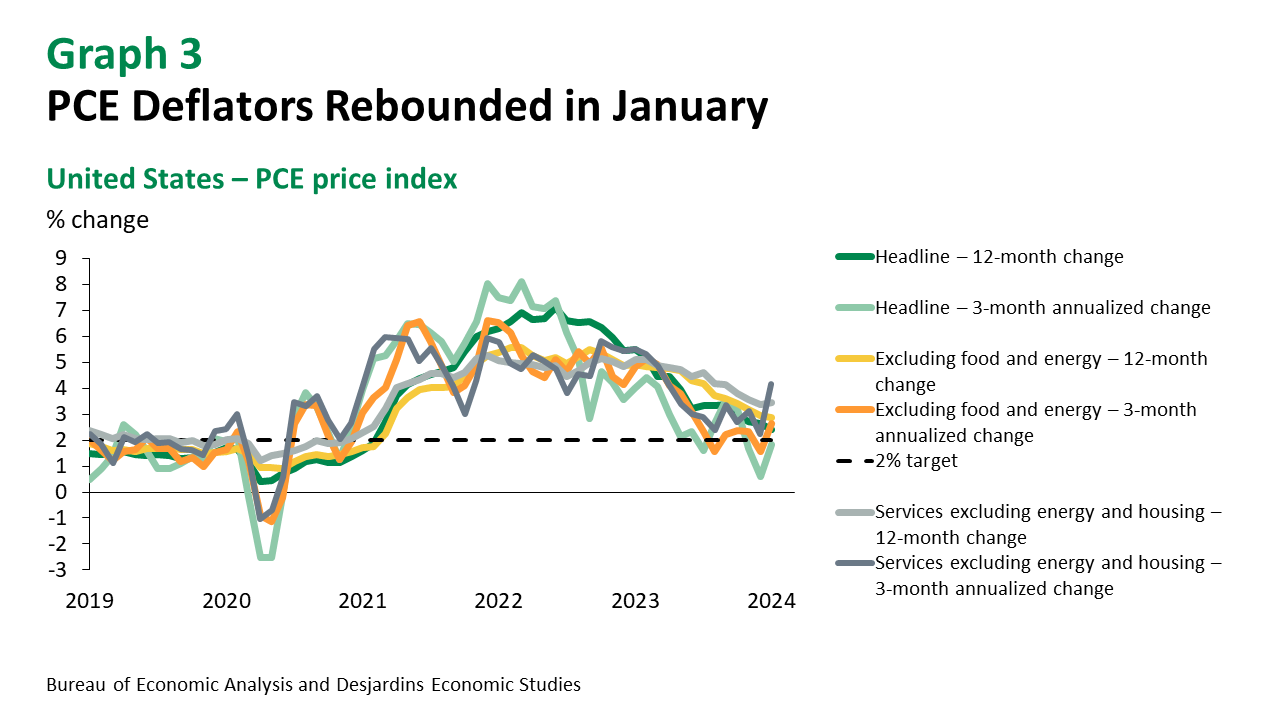

- The Personal Consumption Expenditures price index rose 0.3% in January, while its year-on-year growth slowed from 2.6% to 2.4%. After stripping out food and energy, the PCE price index surged 0.4% month-on-month, with year-on-year growth edging down from 2.9% to 2.8%.

Comments

After US consumers revved up their spending over the last few months of 2023, it was only to be expected that they would start tightening their belts. Last month's slowdown was the first time consumption has cooled since last summer. This seems to be due to the sudden drop in temperatures in January, which contrasted sharply with warm December weather. We've already seen how the cold snap appears to have affected hours worked, retail sales, construction and manufacturing output. As for real consumer spending, goods consumption plunged 1.1%, the biggest drop since November 2022. But the chillier weather also fuelled demand for services, with spending on electricity and gas services soaring by more than 5.5%.

As we've seen, consumption didn't exactly start 2024 with a bang. That said, carryover growth for the first quarter was relatively good. Even if real consumer spending flatlines in February and March, annualized quarterly growth would still come in at 1.6%. But if warmer weather has coaxed shoppers back out, kicking off a rebound in consumer spending in February, we can expect even stronger quarterly growth.

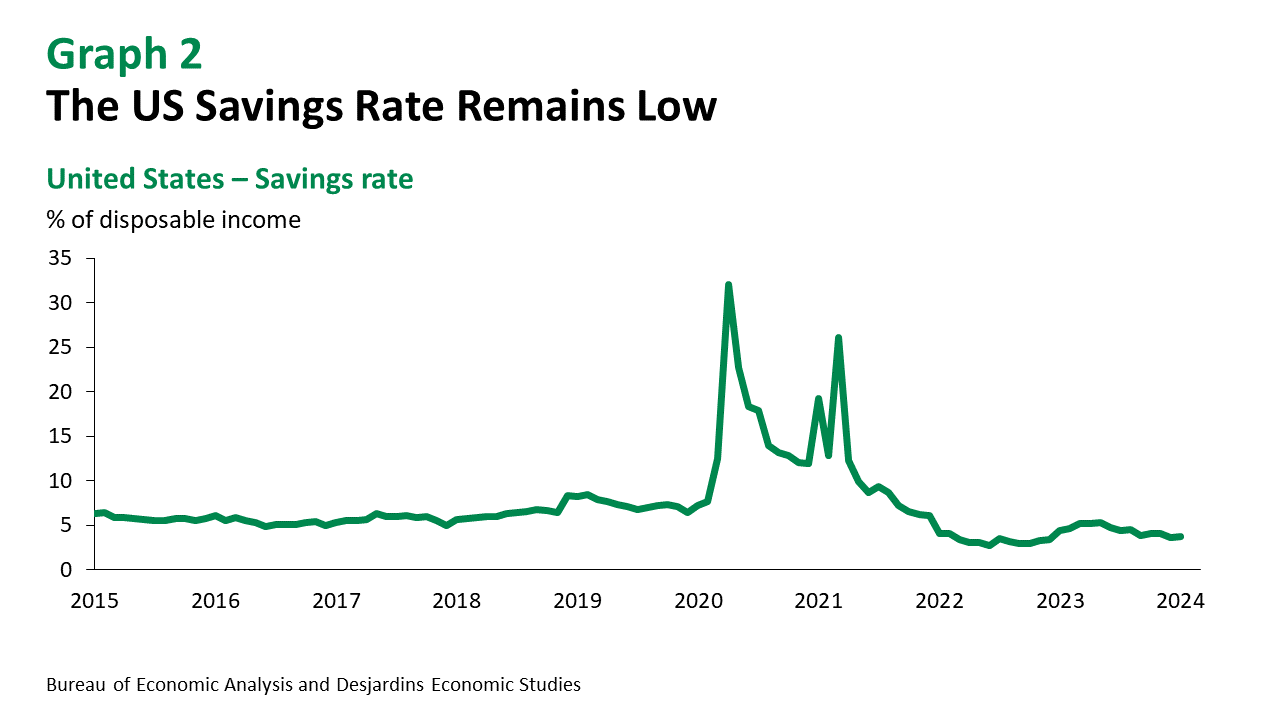

As for US income, January data showed that real disposable personal income plateaued after three months of robust gains. But even though real DPI stayed flat, there were some big changes depending on the source of income. Income from employment went up 0.4% in current dollars, similar to the preceding months. But dividend income ramped up considerably (the biggest jump since December 2020), which boosted total personal income. This was offset by a 6.0% increase in tax payments, which brought real disposable income growth down significantly (and in fact there was no change in real terms). The savings rate inched up from 3.7% in December to 3.8% in January. This is still relatively modest compared to the 2023 average of 4.5%.

Finally, in keeping with the consumer price index, the PCE price index also ticked up in January. The 0.6% rise in prices for services was particularly noteworthy. The 3-month annualized change in the PCE services price index excluding energy and housing—which is one of the key indicators watched by the Fed—accelerated sharply from 2.2% in December to 4.1% in January. This may worry Fed officials.

Implications

After several months of robust growth, the slowdown in real consumption isn't really cause for concern. But the rise in the Personal Consumption Expenditures price index is more likely to worry the Fed. To make sure inflation keeps falling, Fed officials will probably hold off on cutting interest rates for another few months.