- Francis Généreux

Principal Economist

Economic News

US Consumer Prices Come in Hotter than Expected in January

February 13, 2024

Highlights

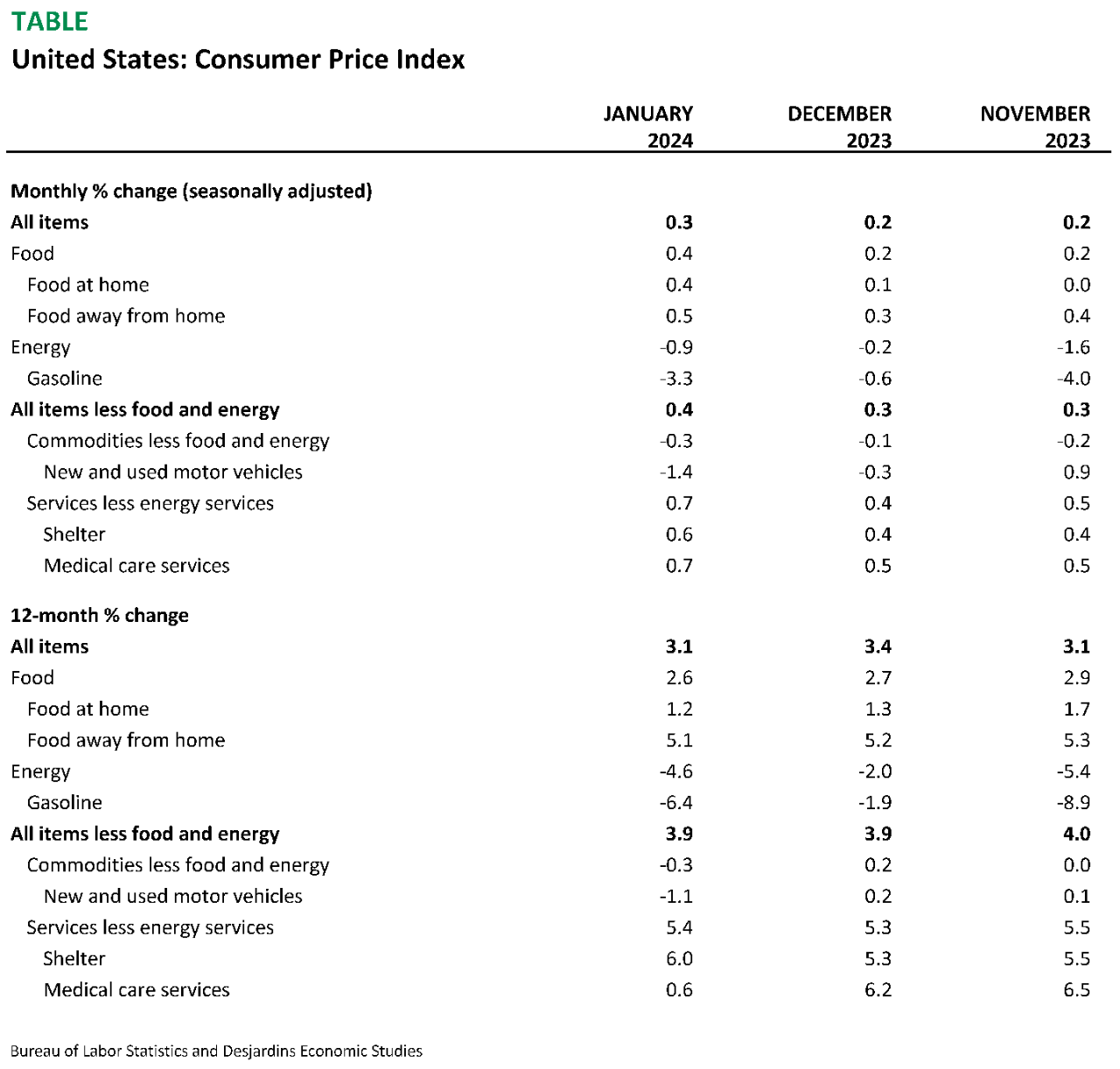

- The US consumer price index (CPI) rose 0.3% in January, after posting two consecutive gains of 0.2% in November and December. Excluding food and energy, it was up 0.4% in January, its biggest jump since April 2023.

- Growth in the all items index nevertheless slowed to 3.1% for the 12 months ending January, down from 3.4% in December. Core CPI increased 3.9%, unchanged from last month.

Comments

Inflation is proving as resilient as the robust US economy. We expected year-on-year growth in consumer prices to slow more in January. We certainly didn't expect the month-on-month change in headline and core CPI to accelerate.

One of the factors that was expected to curtail month-on-month growth in the all items index was energy prices. They did in fact fall 0.9%, due to faltering gasoline (-3.3%) and fuel oil prices (-4.5%). However, after an unseasonably warm December, the January cold snap lifted electricity and natural gas prices. Food prices also popped higher than expected. They advanced 0.4%, doubling the 0.2% gains posted in the preceding two months.

But the biggest disappointment was core CPI, which strips out food and energy. It showed that prices for goods and services are still moving in opposite directions, with goods prices on a downtrend and services prices clearly ramping up in January. For goods prices less food and energy, the month-on-month change was a 0.3% drop in January, the biggest decline since July. Price drops in used cars and trucks and apparel were particularly striking. This was also the eighth month in a row that goods prices sank. For the first time since July 2020, the year-on-year change in goods less food and energy fell into negative territory (-0.3%).

This is in stark contrast to what's going on with prices for services excluding energy. Month-on-month, they jumped 0.7% in January. That's the biggest monthly increase since September 2022. Most of the boost came from housing (+0.6% in January), but also from medical care (+0.7%). Airfares also went up month-on-month (+1.4%). While goods prices plunged year-on-year, services excluding energy climbed to 5.4% in January. That's not as bad as the 7.3% peak hit last year, but it's still too high.

In a US economy that remains surprisingly strong, despite high interest rates, and a job market that's persistently robust, Federal Reserve (Fed) officials may be concerned by how sticky inflation, especially for services, is turning out to be. It will be interesting to see whether the Personal Consumption Expenditures price index—the Fed's preferred metric—will prove to be as resilient as CPI in January.

Implications

The January print is a reminder that the road to lasting 2% inflation is long and winding. The Fed will want to see the CPI slow down even more sharply in the coming months, especially for services. One thing is clear—the possibility of rate cuts at the Fed's next meetings in March and May is becoming increasingly faint.