- Lorenzo Tessier-Moreau, Principal Economist • Hendrix Vachon, Principal Economist

Investment Strategy and Interest Rate Analysis

Policy Rates Are Stabilizing, but Not Long-Term Yields

October 26, 2023

Highlights

- Good news abounds for the US economy.

- Stagnation looms for Canada's economy.

- The US dollar is still weaker than a year ago.

- Rising bond yields are shaking up stock markets.

Economic Conditions and Interest Rates

Good News Abounds for the US Economy

Data released over the past few weeks indicates that the US economy is still far away from a significant slowdown. In fact, it's estimated that US real GDP grew at an annualized rate of 4,9% in the third quarter of 2023. After a few shaky months, employment was up sharply in September, with 336,000 jobs added (graph 1). However, this economic vigor isn't a worldwide phenomenon. The eurozone is showing further signs of a slowdown, and China continues to suffer from weak domestic demand and a troubled property market.

The Federal Reserve Looks Likely to Sit Tight

The Federal Reserve (Fed) previously indicated that a final rate hike could be coming before the end of the year, but in his most recent speech Fed Chair Jerome Powell seemed more inclined to take a wait-and-see approach. US inflation is still too high for the central bank's liking, which justifies maintaining a tight policy stance. However, since the US economy is also being weighed down by the sharp rise in long-term bond yields in recent weeks, there's also an argument for keeping the federal funds rate unchanged.

Stagnation Looms for Canada's Economy.

It's becoming increasingly clear that the Canadian economy is starting to struggle. Highly indebted households have been feeling the squeeze of high interest rates for several months and are cutting back on consumer spending. Despite a pick-up in activity earlier in the year, the housing market had the wind taken out of its sails by recent interest rate hikes (graph 2). Employment continues to rise, but the upward trend is barely tracking the surge in the labour force. Lastly, the recent jump in bond yields could deliver another blow to what is already a fragile economy. Canada looks likely to slip into a recession in 2024.

The Bank of Canada Held Its Key Interest Rate Again in October.

At its October meeting, the Bank of Canada (BoC) kept its key rate unchanged at 5.0% while keeping the door open to further hikes if needed. The Governing Council has indicated that it remains “concerned that progress towards price stability is slow and inflationary risks have increased.” But the Bank also recognizes that “a range of indicators suggest that supply and demand in the economy are now approaching balance.” The expected slowdown of the Canadian economy should reinforce that idea in the coming months, which should ensure status quo for key rates until they start moving back down in 2024.

Retail rates Are Being Influenced by Bond Markets.

The BoC has held its policy rate steady since July, but retail rates have continued to climb (graph 3). 5-year Canadian government bond yields have jumped nearly 50 basis points since the most recent policy rate hike, impacting both mortgage and savings rates. Canada's deteriorating economic outlook is also keeping the cost of funds high for financial institutions, making them favour deposits over loans.

Devises

The US Dollar Is Still Weaker than a Year Ago

At this time last year, amid stock market declines and growing concerns about the economy, the US dollar appreciated considerably thanks to its status as a safe haven. Now the greenback is mainly benefiting from sharply rising bond yields in the United States and widening spreads with the yields of several countries. The fact that the economy appears to be in better shape in the US than in other countries is also good for the greenback. That said, the US dollar isn't as strong as it was last year, at least not against all currencies (graph 4). One of the main differences is that the risk of a European energy crisis has decreased. European currencies are now trading significantly above their fall 2022 lows.

The Canadian dollar is about where it was a year ago. High oil prices haven't been enough to offset the other factors holding back the loonie, such as Canada's worsening economy and widening interest rate spreads with the US. Instead of tracking the spread between 2-year bond yields, the Canadian exchange rate seems more closely aligned with the 10-year bond yield spread (graph 5).

Forecasts

The outlook for the Canadian exchange rate over the coming months remains gloomy. We don't anticipate any significant changes in bond yield spreads that could help the loonie. And oil prices should continue to moderate as the global economy slows. We expect the Canadian dollar to trade around CAN$1.39/USD (US$0.72) this winter.

The yen and several European currencies may appreciate slightly in the coming months as they're less sensitive to oil price fluctuations and stand to benefit more from a decline in US bond yields.

Asset Class Returns

Rising Bond Yields Are Shaking Up Stock Markets

Investors Increasingly Believe Rates Will Stay Higher for Longer.

As mentioned in our previous Retail Rate Forecasts, a period of sustained economic growth could have major impacts on the yield curve and stock markets. Expectations for continued growth seem to have risen dramatically in recent weeks, as evidenced by a strong uptrend in long-term bond yields. In mid-October, the 10-year US government bond yield pushed past the 5.0% mark and has remained volatile since. US and global stocks continue to move lower on these higher yields despite the improved economic outlook in the United States.

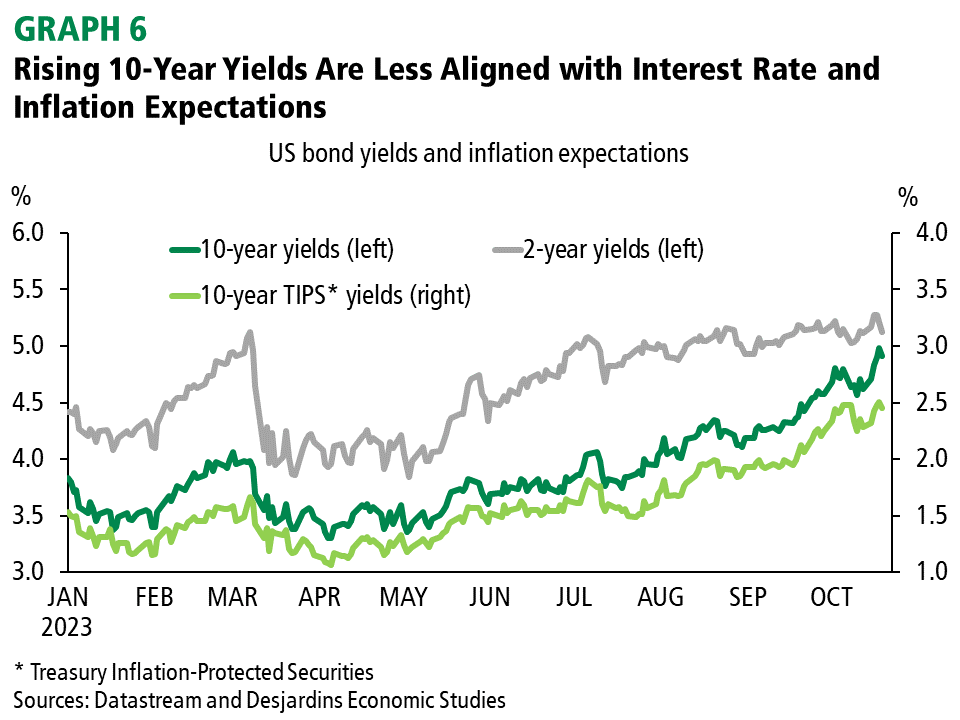

Higher Rates, but Not Necessarily Higher Inflation.

What's interesting about recent bond market movements is that the higher yields don't necessarily reflect increased inflation expectations or a higher risk of central banks raising interest rates further. Long-term yields have risen along with inflation-adjusted rates, but short-term yields haven't done the same. This suggests that investors believe the economy will be able to withstand higher rates (graph 6). The steepening yield curve and introduction of a term premium could also be the result of less liquidity in the financial system after several months of monetary tightening by most central banks around the world.

A Strong US Economy Isn’t Necessarily Good News for Stocks.

Solid economic data has given investors reason to be more optimistic about corporate earnings (graph 7). This partly explains the S&P 500 rally this summer. Rising oil prices late in the summer also drove up earnings expectations for Canada's S&P/TSX. But higher bond yields could have a negative effect on stock market valuations. It now costs significantly more for growing businesses to take out loans and finance expansion, which means their profits need to be that much higher. To compound matters, bonds now offer much better returns, making them a much more attractive alternative for investors.

Canadian Stocks Are Being Battered by Higher Rates While the Economic Outlook Remains Gloomy.

Early fall was a particularly rough patch for the S&P/TSX index, which fell more than 6.0% from its September peak (graph 8). Even though Canada's economic data has been a lot less rosy, its long-term bond yields have kept pace with rising US yields. But fortunately for them, companies on the S&P/TSX have, on average, much lower valuations than their S&P 500 counterparts. The average price-to-earnings ratio is below 13 on the S&P/TSX, while it's around 18 on the S&P 500.

The Global Economic Slowdown Signals the End of Rate Hikes.

There are difficult days ahead for European and Asian stocks as well as US and Canadian stocks. Many countries could slide into a recession in the first half of 2024, if not sooner. Around the world, it seems the end of monetary tightening is at hand. The European Central Bank hit the pause button in October. But another rate hike is still likely in the United Kingdom, where inflation continues to run high. The Bank of Japan’s next move is unclear. It could have started monetary tightening, but hasn't yet. It will probably announce one or two 10 basis-point hikes soon, just enough to bring its policy rate slightly above 0%. On top of the recently loosened yield curve control, this could give the yen a boost and help curb inflation. That said, a stronger yen could hurt Japanese stocks.

Return Potential Is Improving in Bond Markets.

Anyone with stocks and bonds in their portfolio will probably want to forget September and October 2023. But there's hope on the horizon thanks to rising bond yields. As yields rise, the odds of further increases go down and future return potential goes up (graph 9). That said, high bond yields are an additional risk for stocks.

Contactez nos économistes

Par téléphone

Montréal et environs :

514 281-2336 Ce lien lancera votre logiciel de téléphonie par défaut.