- Jimmy Jean, Vice-President, Chief Economist and Strategist

Lorenzo Tessier-Moreau, Principal Economist • Hendrix Vachon, Principal Economist

Investment Strategy and Interest Rate Analysis

Canada Gets Closer to Cutting Rates, but the US May Have to Hold Off

May 7, 2024

Highlights

- The US economy is still generating too much inflationary pressure.

- The Bank of Canada took another step towards its first rate cut.

- The prospect that monetary policies could diverge sent many currencies lower against the US dollar in April.

- The jump in bond yields is hampering positive stock market momentum.

Economic Trends and Interest Rates

The US Economy Is Still Generating Too Much Inflationary Pressure

Although economies all over the world are showing some signs of weakness, the US is showing fewer signs than most. In the first quarter, real GDP disappointed forecasters by growing an annualized 1.6%. But US domestic demand remained stubbornly high, increasing 2.8% over the same period. The soft GDP growth was the result of a sharp increase in imports and a decline in inventory, which are both further evidence of the strength of US consumer demand. More importantly, price gains, as reflected by the Personal Consumption Expenditures deflator, clearly show the persistence of inflationary pressures in the United States (graph 1).

The Fed Is Dissatisfied with the Progress on Inflation

At its May 1 meeting, the Federal Reserve (Fed) noted that there has been a lack of further progress on inflation in recent months. This suggests that we shouldn’t expect rate cuts in the short term. But, even though some Fed officials have raised the idea, the press release for the meeting didn’t open the door to rate hikes. The Fed continues to suggest that its next move will be a cut, but it will need to have greater confidence that inflation is moving sustainably towards 2% before that can happen. The meeting did mark the central bank’s first change to its monetary policy. It decided to reduce the monthly cap on the amount of federal bonds it allows to roll off its balance sheet, from US$60 billion to US$25 billion. It seems increasingly clear that the Fed won’t feel ready to start cutting rates before the fall.

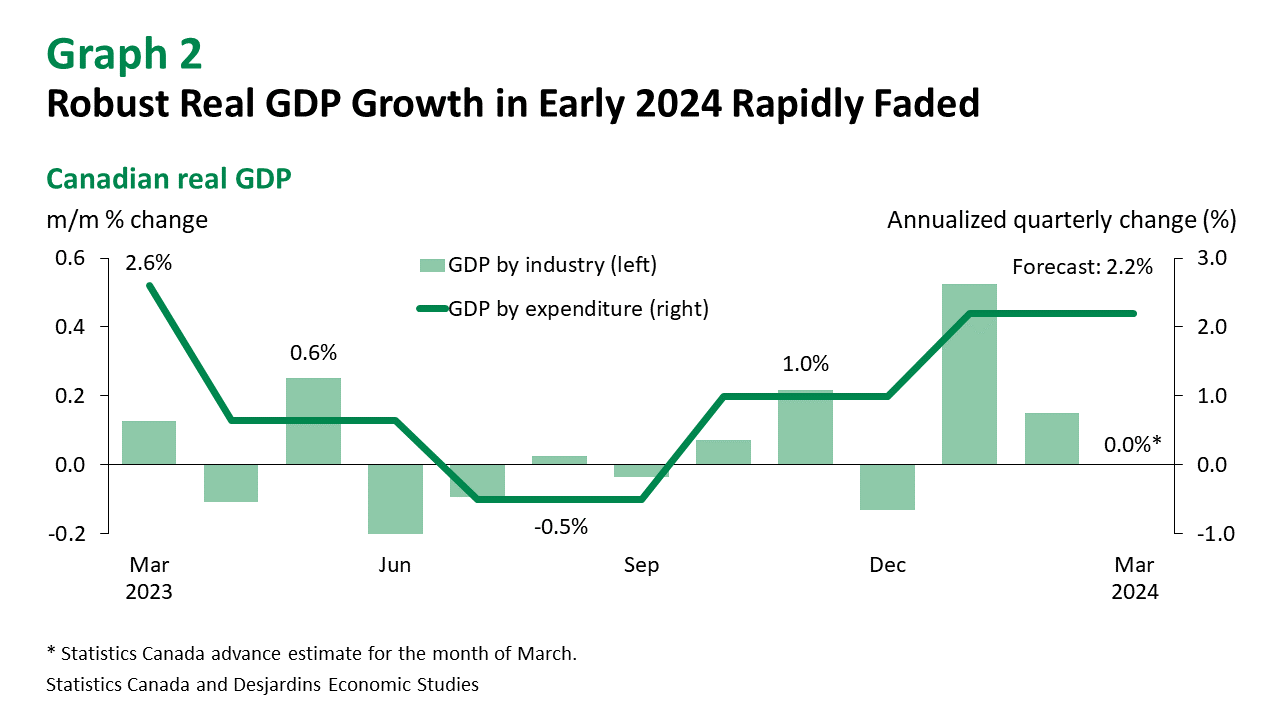

The Canadian Economy Kept Growing at the Start of the Year

Canadian real GDP continued to expand in early 2024. Following a sharp rebound after the Quebec public sector strikes ended in January, GDP by industry lost momentum in February and March (graph 2). This return to slower growth better reflects the trends observed in other indicators. In particular, the jobs market continued to soften, as employment stayed flat in March. Furthermore, sustained population growth helped drive unemployment up to 6.1%, a high not seen since 2022. The problems with the Canadian economy are also reflected in inflation numbers, which remain decidedly weaker than in the United States.

The Bank of Canada Took Another Step towards Its First Rate Cut

The latest inflation readings seem to have reassured the Bank of Canada (BoC). During the BoC’s April 10 meeting, it presented a potential path towards the first key rate cuts. During the press conference, BoC Governor Tiff Macklem said, “We are seeing what we need to see, but we need to see it for longer [to be convinced it’s time to cut rates].” But this message was somewhat undermined by an upward revision of the BoC’s economic forecast. The progress made on inflation could make it possible for the BoC to start cutting its overnight rate in June, but stronger growth and tighter US monetary policy could slow down the rhythm of subsequent cuts.

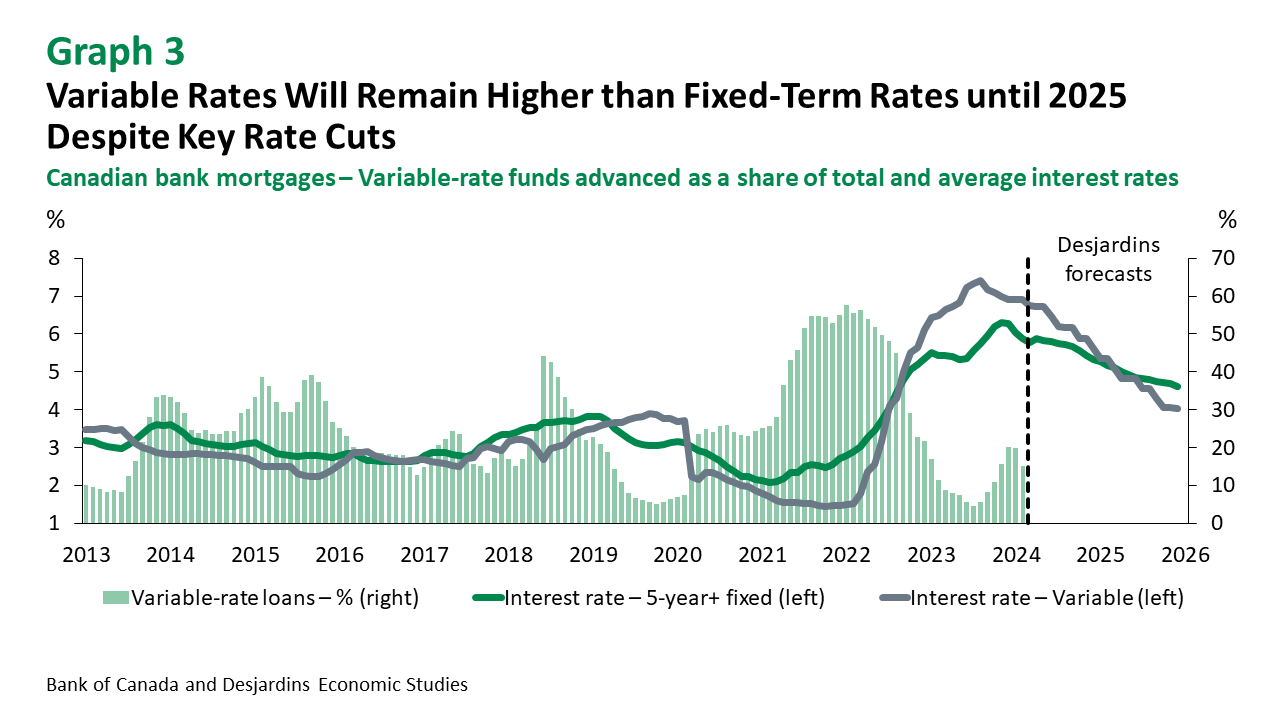

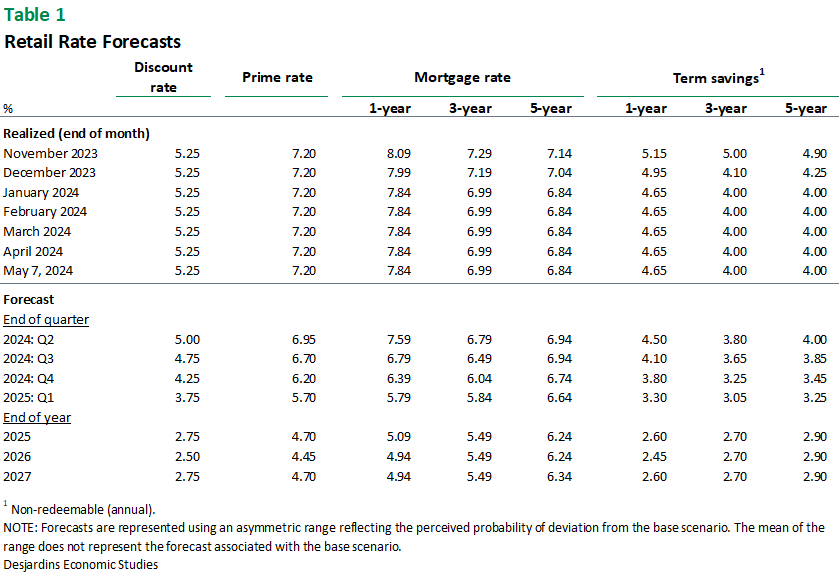

Lower Key Interest Rates Won’t Have Much of an Impact on Retail Rates

Borrowers may be pleased to see key rates start coming down, but it’s important to bear in mind that this won’t affect all retail rates. Rates will go down for products with variable interest rates, but since most of these are higher than longer-term fixed rates, borrowers may not find them particularly attractive at the moment (graph 3). Fixed-term retail rates are much more heavily influenced by bond yields. They don’t just rise and fall based on national monetary policy. They’re also affected by the economic outlook outside of Canada and by international bond markets. The recent rise in long-term bond yields could therefore keep retail rates higher for several months.

Exchange Rate

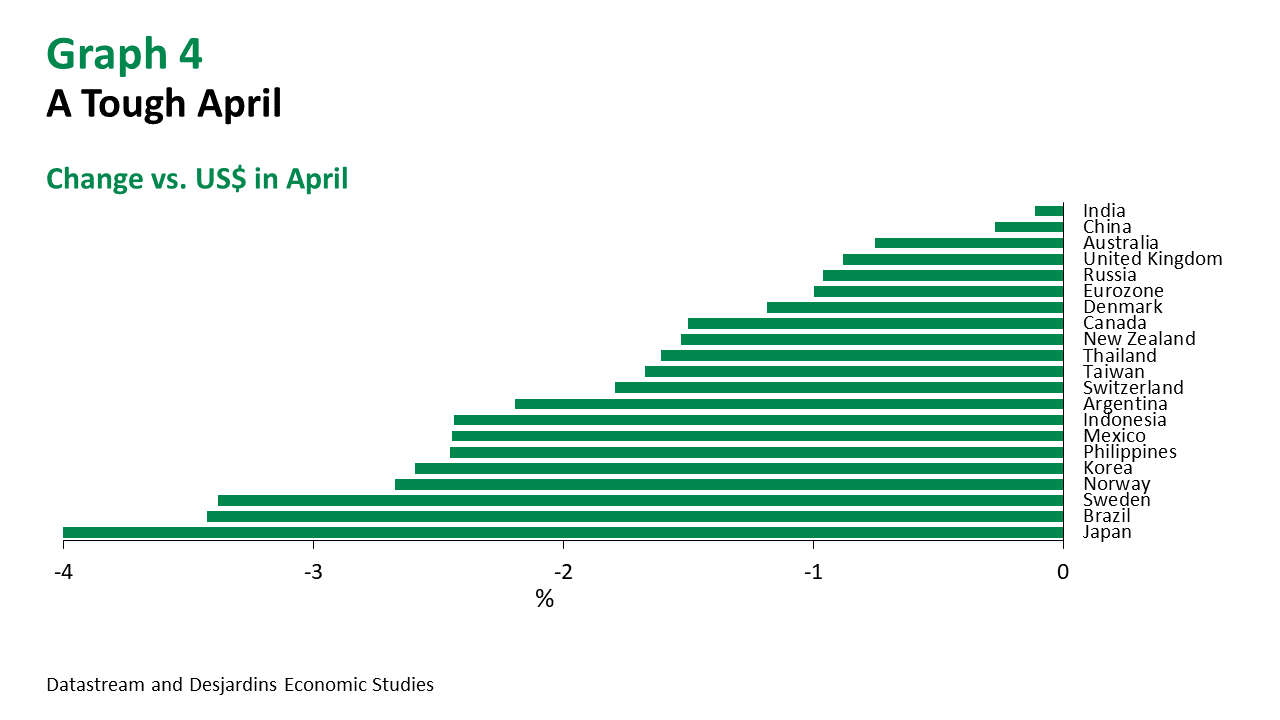

The Prospect that Monetary Policies Could Diverge Sent Many Currencies Lower Against the US Dollar in April

Currency Shock after US Inflation Reading

As with bond yields, there were a lot of changes in exchange rates in April after US data showed just how sticky inflation is (graph 4). In general, emerging market currencies fell the most. The rise in US bond yields has added another layer of financial stress for many of these countries since they typically borrow in US dollars. Mexico and Brazil were among those that saw their currencies depreciate the most. The fact that both countries’ central banks had already started lowering their key interest rates added to the downward pressure on these currencies. The yen also took a big hit, as the spread between Japanese and US yields remains wide.

The Loonie Didn’t Fall as Much as Some Other Currencies

The Canadian dollar lost just over 1% in April, though at one point during the month it was down more than 2%. Investors still aren’t betting on Canada’s monetary policy diverging significantly from the US’s, but interest rate spreads between Canada and the United States widened nonetheless. The slump in oil prices didn’t have too much of an impact on the Canadian dollar, which also barely budged during the preceding uptick in crude prices.

The Canadian Dollar Could Soon Put the C$1.40/US$ Threshold to the Test

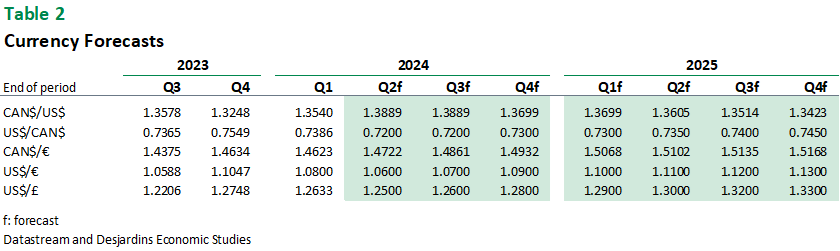

May and June will probably look a lot like April. Changing monetary policy expectations will likely continue to shake up the currency market. Our new forecasts for the Federal Reserve and the Bank of Canada are consistent with interest rate spreads widening in the coming months and the Canadian dollar depreciating further (graph 5). The markets still haven’t fully priced in the two interest rate cuts that we expect in Canada in June and July. The loonie will likely get close to the C$1.40/US$ threshold over the summer. But it could start recovering by the fall, in anticipation of US rate cuts.

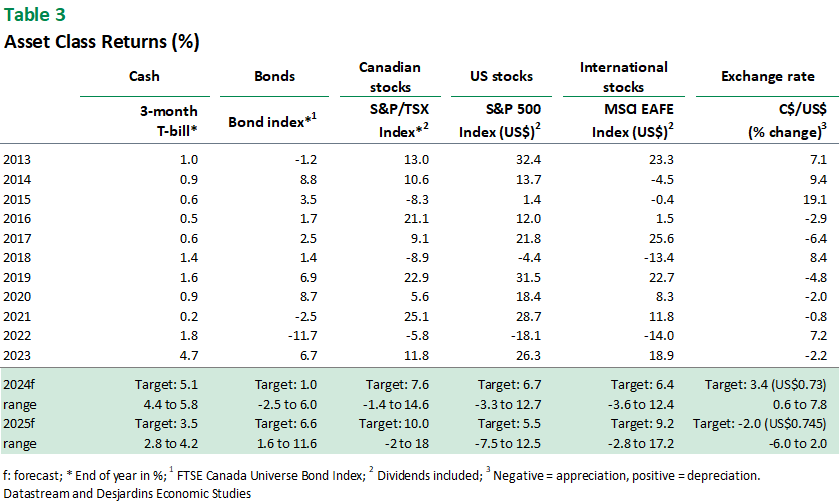

Asset Class Returns

The Jump in Bond Yields Is Hampering Positive Stock Market Momentum

Government Bond Yields Are Approaching October Highs

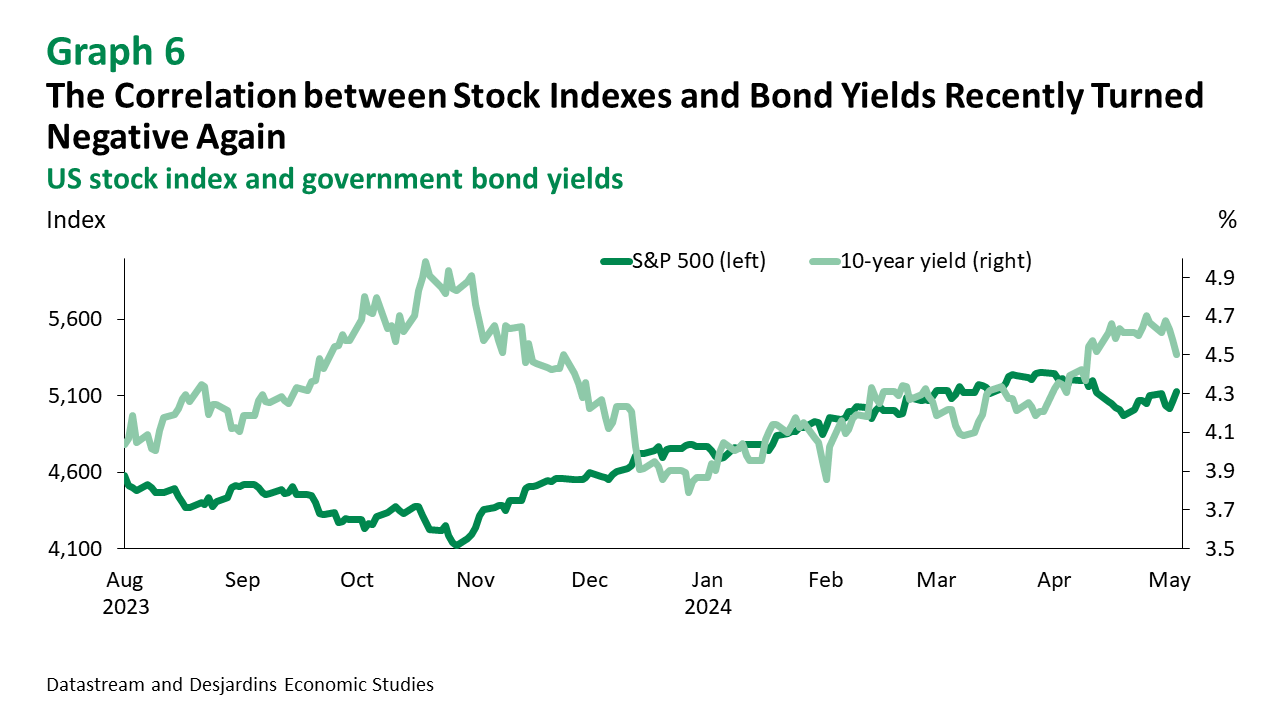

Bond returns were once again hit by rising yields. The resurgence of inflationary pressures in the United States led market participants to sharply revise their forecasts for key rates. This had an impact that could be seen throughout the yield curve. The uptick in yields also sent a wave of uncertainty through the stock markets, which fell sharply in April (graph 6). Investors seem to have been reassured by Fed Chair Jerome Powell’s messaging in early May, which helped stabilize bond yields and sent markets back up a few points. But it’s too early to say whether this trend will last.

Stock Markets Have Temporarily Stopped Rising—and for Good Reason

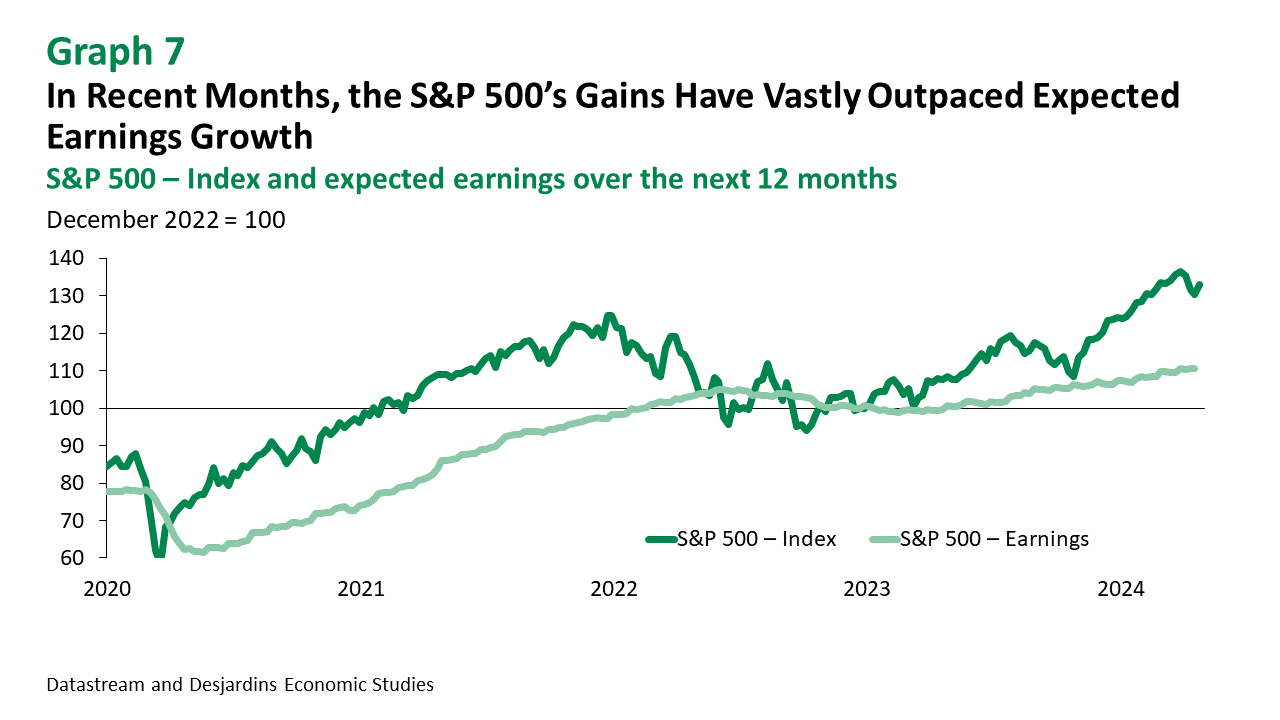

The recent stock market decline shouldn’t surprise anyone, especially in the United States. The S&P 500 had been on an almost uninterrupted 5-month winning streak fuelled by the tech craze and optimism over economic growth and inflation. The stock market boom pushed share price growth far above that of expected corporate earnings (graph 7). The recent improvement in the economic outlook suggests corporate earnings will continue to rise, but it could also keep interest rates higher for longer. This could make it hard to justify today’s high stock valuations.

Canadian Equities Benefit from Monetary Policy Divergence and Lower Stock Prices

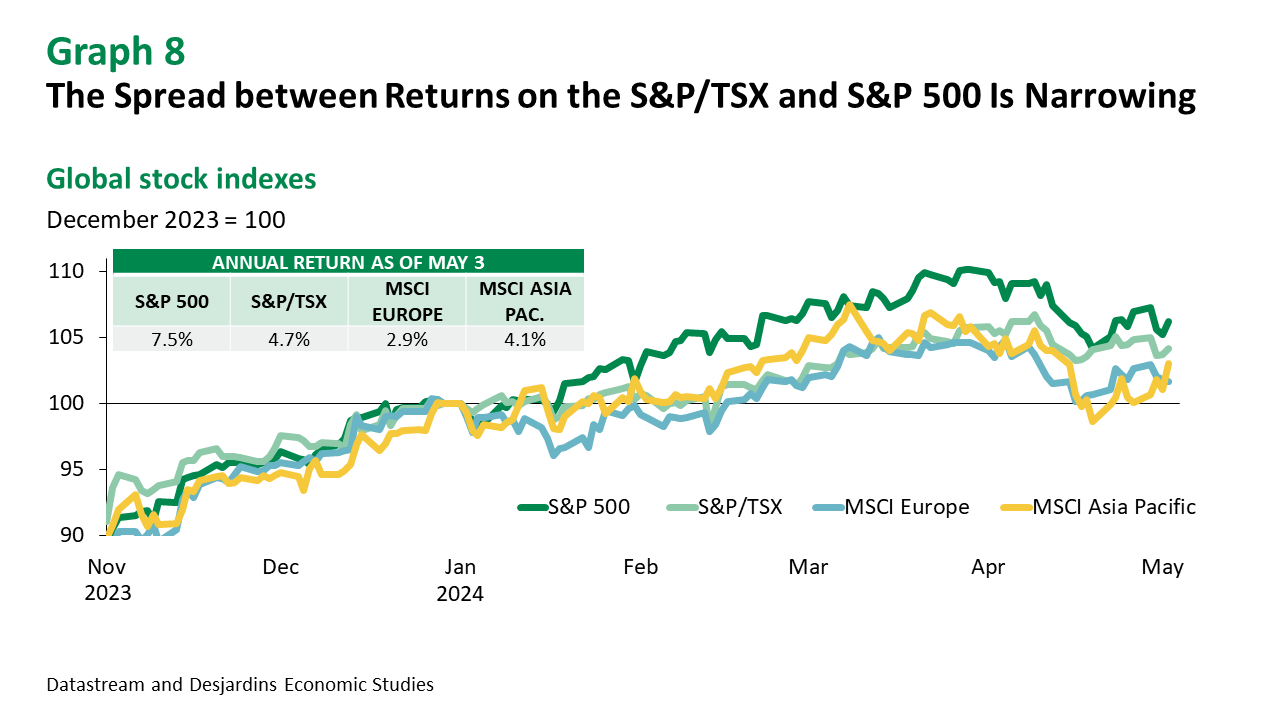

Although forecasts for US key rates have been revised upward, the economic outlook for Canada is much gloomier. This would justify looser monetary policy and a weaker loonie. Both of these factors could lift Canadian corporate earnings by driving up demand for exports and reducing borrowing costs. Relatively lower interest rates could also push up stock prices. These factors, along with a boost from certain commodity prices, helped limit the recent drop in the S&P/TSX index (graph 8). This means that, despite tougher economic conditions, Canada’s flagship index could very well outperform the S&P 500 in 2024.

The European Central Bank Set the Stage for a Rate Cut in June

Investors everywhere are betting that the European Central Bank (ECB) will start cutting rates in June. Progress on inflation and lagging economic growth have kept the eurozone in disinflationary territory. In April, the ECB gave a strong signal that it could cut rates in June. As for the United Kingdom, the Bank of England (BoE) will most likely wait a little longer, until it sees signs of further progress on inflation. We expect the BoE to start cutting rates at its early August meeting, which would fall between the first cuts made by the Fed and ECB.

Meanwhile, the yen’s depreciation is cranking up the pressure on the Bank of Japan (BoJ) to raise rates. We expect it to announce two interest rate hikes by late summer. The BoJ could also intervene on forex markets to prop up the yen and keep import prices from fuelling inflation. But even though monetary policies in Asia and Europe are diverging from the Fed’s, it wasn’t enough to limit the global stock market decline since the risks related to corporate earnings seem to be bigger.

Big Risks Remain for Stock and Bond Markets

If there’s one thing we should learn from the events of recent weeks, it’s that interest rate forecasts can change fast. In just a few weeks, investors went from expecting three cuts to the fed funds rate in 2024 to only expecting one. Inflation is still very much a risk, as shown by recent US figures. If this risk materializes, forcing the Fed to start raising rates again, it’s quite possible we’d see further sharp downturns on both stock and bond markets. Our baseline scenario still expects some stock market volatility over the short term, followed by a recovery in the second half of the year. We also predict bond yields will start heading back down, boosting returns for this asset class.