- Jimmy Jean, Vice-President, Chief Economist and Strategist

Lorenzo Tessier-Moreau, Principal Economist • Hendrix Vachon, Principal Economist

Investment Strategy and Interest Rate Analysis

Doubts about the US Economy Have Sparked Market Volatility

August 15, 2024

Highlights

- As inflation slows, economic growth has become a concern once again.

- Lower interest rates will provide a bit of relief to the Canadian economy.

- Times are tough for many commodity-linked currencies.

- Volatility has returned to global markets.

Economic Trends and Interest Rates

As Inflation Slows, Economic Growth Has Become a Concern Once Again

Around the world, inflation data continued to move in the right direction over the summer, prompting some central banks—including those in Canada and the eurozone—to start cutting their key rates. However, fears have resurfaced about how past interest rate hikes could still be hurting economic growth, particularly following the release of disappointing US employment data for July. Concerns were sparked by the unemployment rate jumping to 4.3%, as the increase exceeded the Sahm Rule threshold,1 which has accurately signalled the start of past recessions (graph 1). However, it could be an imperfect signal as the rise in unemployment is due in part to labour force growth. We still believe that a recession can be avoided in the United States. It’s important to keep in mind that second-quarter GDP growth once again surprised to the upside in both the US and the eurozone.

1 Created by US economist Claudia Sahm, the Sahm Rule stipulates that historically recessions have begun when the 3-month average of the unemployment rate exceeds the 12-month low by 0.5%.

The Federal Reserve (Fed) Held Rates in July but Signalled That Cuts Are Coming in September

The Fed might have made a different decision if it had already seen the July employment data—but those numbers were only published two days later. Despite maintaining its key interest rate, the central bank was more accommodating in its press release for the July 31 meeting. Notably, it expressed greater concern about the state of the labour market. The Fed also indicated it’s now more confident that it has made headway in bringing down inflation and that going forward it will be attentive to both sides of its dual mandate (employment and inflation). However, this message wasn’t enough for investors, some of whom now believe that the US rate-cutting cycle may need to kick off with a 50-basis-point adjustment. Our view is that fears about the US economy aren’t entirely justified and that there will be a 25-basis-point reduction in September, with subsequent cuts to follow.

Lower Interest Rates Will Provide a Bit of Relief to the Canadian Economy

Canada’s economy is still managing to eke out feeble gains despite the high interest rates that have prevailed for several months. Advance and official information on real GDP by industry suggest that GDP by expenditure expanded at an annualized rate of roughly 2% in the second quarter, following a 1.7% gain in the first quarter. With this growth rate, job creation isn’t keeping up with the needs of the country’s fast-growing labour pool. As a result, unemployment has been steadily rising for several months (graph 2). While the recent interest rate cuts could help, it will take time for them to work their way through the economy as a whole.

The Bank of Canada (BoC) Cut Rates Again and Further Reductions Now Seem More Certain

After reviewing the latest economic data, the BoC moved forward with a second consecutive policy rate reduction in July, trimming it to 4.5%. And while the accompanying press release didn’t explicitly signal further cuts, the reading it provides of the Canadian economy makes things crystal clear. Speaking on the topic, the Governor of the BoC said, “the economy has more room to grow without creating inflationary pressures.” The BoC could also be influenced by the change in US data, which opens the door to additional back-to-back policy rate cuts in the coming months.

Pressure on Borrowers Is Easing

We expect the BoC to have slashed its policy rate to 3.75% by the end of 2024 and 2.25% by the end of 2025. This means that variable interest rates should keep coming down over the coming months, moving in lockstep with the policy rate. Fixed interest rates have been lower than variable rates for the past several months, and they will likely continue to edge lower by following roughly the same trajectory as bond yields. Fixed rates could therefore remain lower than variable rates for several more months. Even though we expect the policy rate to shed more than 200 basis points by 2025, interest rates for 5-year fixed-term loans could fall less than 100 basis points due to more modest movements in the bond market (graph 3). We covered this topic in detail in a recent Economic Viewpoint External link..

Exchange Rate

The Canadian Dollar Remains under Pressure

Times Are Tough for Many Commodity-Linked Currencies

In recent weeks, concerns about global demand have weighed on commodity prices. This hurt a number of currencies, including the Canadian dollar. However, the loonie has fared comparatively better than other commodity-linked currencies like the Australian dollar (graph 4).

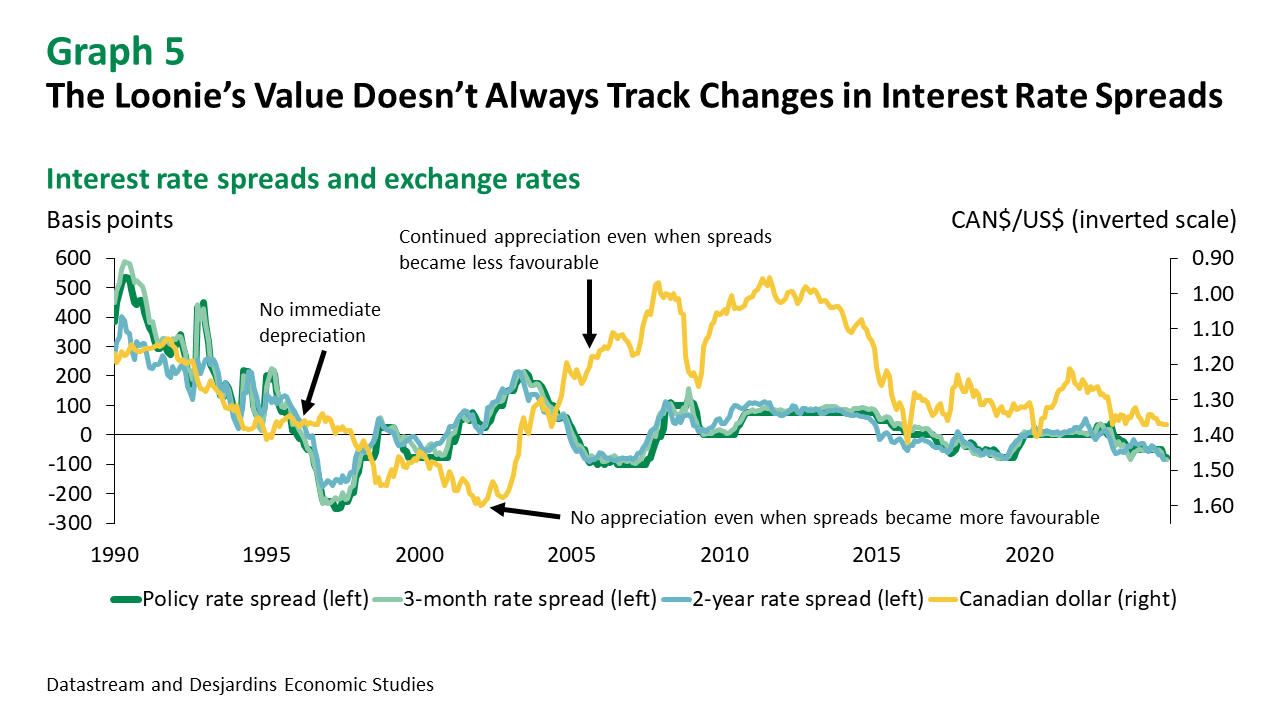

Canada’s Falling Interest Rates Won’t Necessarily Crush the Loonie

The Bank of Canada’s July decision to continue cutting interest rates could have sent the Canadian dollar lower against other currencies. But this was tempered by the US dollar weakening against a number of currencies as market expectations shifted toward more aggressive interest rate cuts in the United States. But as we explained in a recent Economic Viewpoint External link., the Canadian exchange rate isn’t strictly tied to interest rate spreads with the US (graph 5). The Canadian dollar is more likely to take a hit if the economy struggles, if oil and other commodity prices fall, or if there’s financial turmoil in the markets. During the worst of the recent market volatility, the loonie came close to CAN$1.39/US$, but it subsequently appreciated to better than CAN$1.38/US$.

The Trend Will Reverse Next Year

The Canadian dollar will likely hold steady at around CAN$1.38/US$ for the next few months. After that, a slight appreciation is expected, supported by an improved economic outlook in Canada and several other countries, as well as continued high prices for oil and other commodities.

The Yen Has Surged

Of all currencies, the yen has seen its value change the most. In early July it was over ¥160/US$ but it’s now trading around ¥147/US$. For a long time, the Bank of Japan (BoJ) maintained an ultra-loose monetary policy, with massive asset purchases and negative interest rates. But things have finally started to shift. The BoJ has been scaling back on asset purchases and in July it raised interest rates for a second time. Although the US/Japan interest rate spread is still wide, it no longer justifies such a weak yen. The Japanese currency could continue to appreciate in the coming quarters.

Asset Class Returns

Volatility Has Returned to Global Markets

Global Stock Markets Have Been Hit Hard by Renewed Recession Fears

The release of US employment data triggered tumult in global stock markets. Amidst recession fears, government bond yields slid significantly further in early August, sparking serious financial volatility, especially on Monday, August 5. With US Treasury yields falling and the yen surging, the Japanese Nikkei 225 tumbled more than 12%, with repercussions on global markets. The indexes have since recovered much of that lost ground, but they’re still below their recent highs. The correlation between stock market returns and bond yields has turned negative again (graph 6). Investors seem to be looking beyond shifts in monetary policy and have turned their attention back to recession risks and corporate earnings.

Corporate Earnings Are Still on the Rise

One of the reasons stock market returns have been so strong since the beginning of the year is that corporate earnings expectations have been trending upward, particularly in the United States and Canada (graph 7). Thanks to these stronger earnings, Canadian stock valuations remain relatively attractive, even though prices have increased since the beginning of the year. But the same isn’t true for S&P 500 stocks, especially those in the tech sector. Even with the continued rise in earnings and strong growth prospects, the US index still seems to be greatly overvalued compared to historical levels (graph 8).

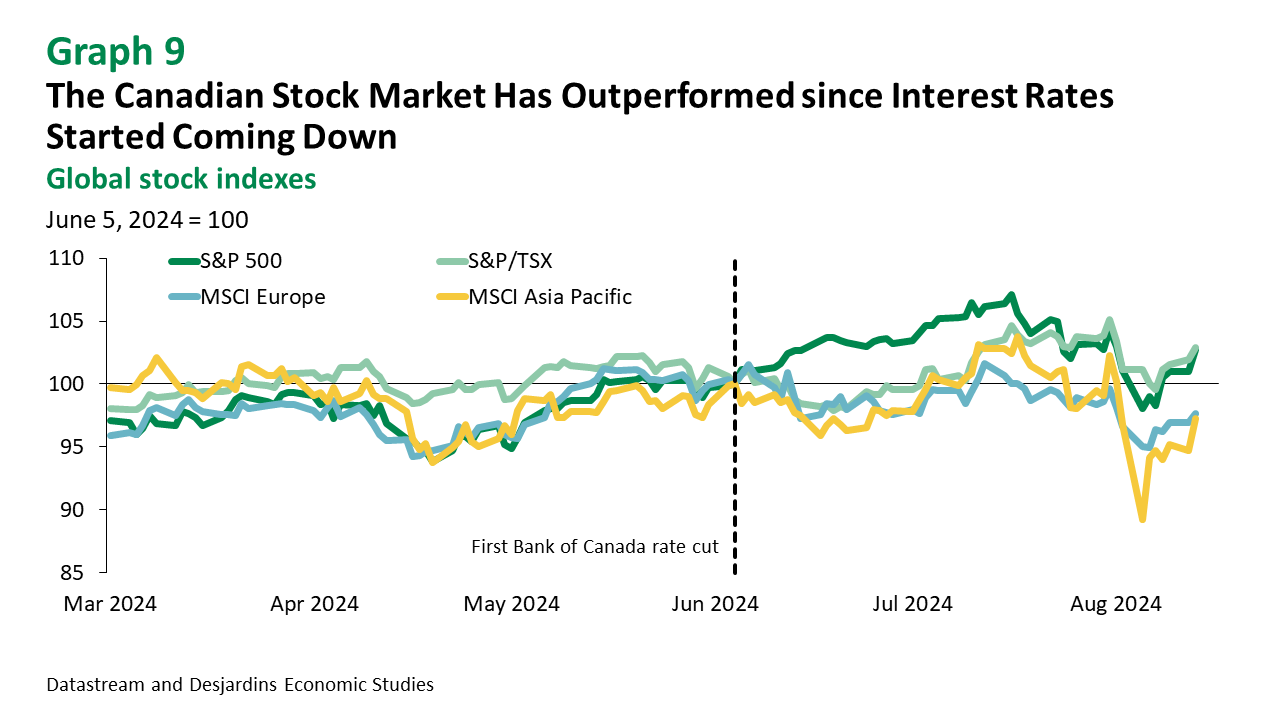

The Canadian Stock Market Seems to Be Benefiting from the Effect of Rate Cuts

The Bank of Canada started its monetary easing cycle ahead of other major central banks and has already made two successive policy rate cuts. Its rate decisions and dovish tone have driven up both bond yields and stock market returns. While it’s true that the S&P/TSX declined along with other global stock markets in early August, its fall wasn’t as steep and the index has performed relatively well since the rate-cutting cycle began (graph 9). But despite the interest rate reductions, the Canadian economy’s growth prospects remain fairly bleak, and this could limit the index’s gains by the end of the year.

Monetary Policy Remains a Concern for Other Global Markets

In Europe, stalled progress on inflation is forcing the European Central Bank (ECB) to take a cautious approach. After making an initial rate cut in June, it decided to leave rates unchanged in July. But another cut is likely to come in September if the ECB’s updated inflation projections indicate that things are moving in the right direction. The Bank of England announced its first rate cut on August 1, following a narrow vote with just 5 out of 9 members of its monetary policy committee in favour. The opposing members were concerned that inflation risk is still too high. Like in the eurozone, the pace of further cuts will likely be gradual and uncertain, which could continue to fuel market volatility.

An Appreciating Yen Spells Trouble for Japan’s Stock Market

After several months of weakness, the yen abruptly shot up following the Bank of Japan’s meeting on July 31. At the same time, the Nikkei 225 plummeted in anticipation of lower exporter profits and the unwinding of the so-called carry trade, in which investors borrow at low interest rates in yen to invest in higher-yielding currencies elsewhere. In fact, the unwinding of the yen carry trade seems to have been one of the main catalysts for the high volatility observed in early August.

Greater Stock Market Volatility Could Be on the Horizon for the Second Half of 2024

Now that most major central banks have started cutting interest rates or confirmed their intentions to do so, a cloud of uncertainty has been lifted from the stock and bond markets. But that doesn’t mean the skies have cleared. The return of US recession fears are a case in point. The US presidential election and the escalating conflict in the Middle East could also spark more uncertainty and volatility. Although we don’t anticipate a US recession, we believe that risks persist for stock market returns. In addition, the world’s leading economies slowed over the last year, which could crimp corporate profits. US stock valuations are near their cyclical peaks, which sets the bar very high for future earnings growth.