- Lorenzo Tessier-Moreau, Principal Economist • Hendrix Vachon, Principal Economist

Investment Strategy and Interest Rate Analysis

Rate Cuts on the Horizon for 2024

December 7, 2023

Highlights

- The United States May Avoid a Recession

- Canada's Economy Has Hit a Soft Patch

- Despite the Canadian Dollar's Recent Appreciation, There Isn't Much to Support Future Gains

- The Possibility of a Soft Landing for the US Economy Soothes Investors

Comments

The United States May Avoid a Recession

After more than 20 months of monetary tightening, there is now no denying that inflation is stabilizing worldwide (graph 1). It remains above target in many countries, but recent trends and leading indicators suggest that central banks could soon go back to cutting key rates. Despite all this, the US economy has continued to post sustained growth in 2023, and although it is cooling, signs of weakness have been minimal so far. But even if this economic slowdown persists, we believe the United States could be one of the only advanced economies to sidestep a recession in 2024.

The Federal Reserve Is Gradually Opening the Door to Future Rate Cuts

Although the Federal Reserve (Fed) has stated that its policy decisions at future meetings will be based on all the data available at the time, it's becoming increasingly obvious that the status quo should last for a while. Some members of the Federal Open Market Committee have even started dropping hints about the conditions that could potentially lead them to lower the fed funds rate in 2024. We expect the downshift in inflation to give the Fed room to start cutting its key rate in the second half of next year.

Canada's Economy Has Hit a Soft Patch

Canadian real GDP fell at an annualized rate of 1.1% in the third quarter, while the labour market continued to slacken. Even though employment rose in recent months, the labour force grew even more, driving unemployment up to 5.8%. The job vacancy rate is now close to where it was before the pandemic (graph 2). The weakness in Canada's economy can be seen in many sectors. While there may be a slight rebound in the fourth quarter, we expect the economic contraction to persist into early next year.

The Bank of Canada May Start Cutting Rates Again in the Spring

As expected, the Bank of Canada (BoC) left its key rate unchanged in December. The press release for its latest meeting highlighted the Bank’s belief that “the economy is no longer in excess demand” although it “is still concerned about risks to the outlook for inflation.” The BoC continued to play it safe by leaving the door open to more rate hikes, but the conditions for rate cuts may be in place next year. However, the central bank is expected to lower rates gradually unless a recession hits the Canadian economy much harder than expected.

Retail Rates May Have Finally Peaked

Posted rates on mortgages and savings hit record highs in October on the back of a spike in bond yields (graph 3). But yields fell again in November, giving borrowers some relief and suggesting—for the first time in two years—that interest rates offered to customers may finally start going down. As with policy rates, we expect retail rates to go down slowly in the coming months. That said, financial institutions may choose to further limit how much credit they grant if economic conditions keep deteriorating.

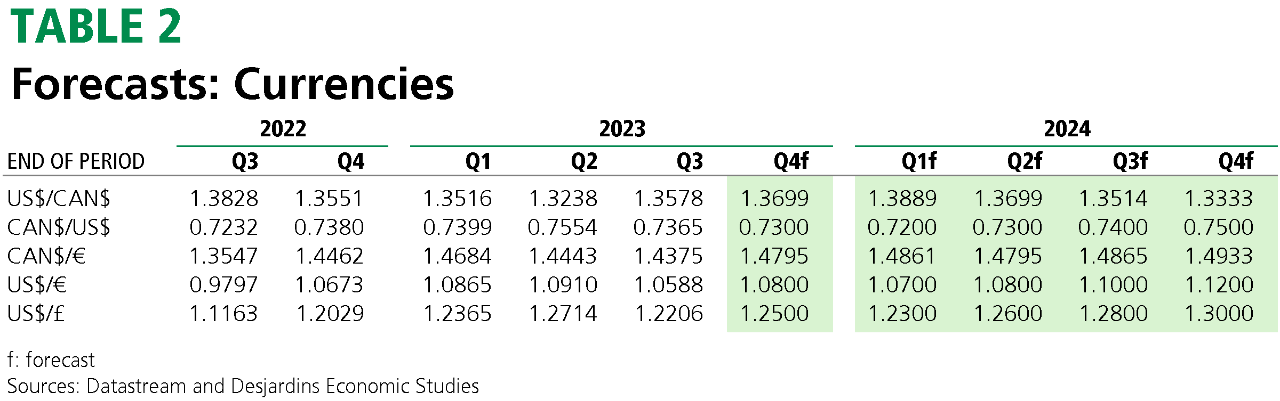

Exchange Rate

Despite the Canadian Dollar's Recent Appreciation, There Isn't Much to Support Future Gains

Highlights

November saw many currencies appreciate against the US dollar. This was driven primarily by the drop in bond yields, which was especially steep in the United States. Renewed risk appetite also exacerbated the greenback's overall weakness. The DXY US Dollar Currency Index is back to where it was in late August (graph 4).

The Canadian dollar was one of the currencies that posted the smallest gains against the greenback in November (graph 5). The loonie's rise got more traction mid-month, after US inflation data and several more encouraging economic indicators for the Chinese economy were released. Those numbers sharpened investors' risk appetite. The Canadian dollar didn't benefit as much as other currencies from the pullback in US yields, since Canadian yields fell by a similar percentage. Low commodity prices and downbeat Canadian economic data also weighed down the loonie.

Forecasts

Changes in risk appetite are likely to drive most currency fluctuations in future months, while variations in yields are expected to have less of an impact. Our baseline scenario sees many countries experiencing economic hardship over the short term, which would cause risk appetite to wane. This should drive up demand for the US dollar.

Meanwhile the Canadian dollar remains highly sensitive to investor sentiment and the state of the global economy. We believe that in the short term it will slip down to around US$0.72 (C$1.39/US$) before going back up later in 2024. The loonie's rebound will coincide with an economic recovery and a run-up in commodity prices.

Asset Class Returns

The Possibility of a Soft Landing for the US Economy Soothes Investors

Stock Markets Rise on Lower Bond Yields

After peaking in October, long-term bond yields fell all through November (graph 6). As yields dropped, the major stock indexes rebounded sharply. Investor optimism is somewhat justified. Recent data suggests that inflation may be tamed without tipping the US economy into recession. Investors have therefore welcomed weaker economic readings as further evidence that key rates could eventually be cut. These expectations appear to have been confirmed by the Fed's latest messaging.

Tech Stocks Are Still Leading the Pack

As has been the case for most of the past year, the recent surge in the S&P 500 US stock market index was largely driven by a few big companies in the tech and communications sectors. Gains have been so heavily concentrated in these stocks that if we eliminate the index's top 7 companies in terms of market capitalization, its annual increase as of November 30 would plunge from more than 18.0% to just below 6.0% (graph 7). The Magnificent Seven's exposure to advances in artificial intelligence were the main reason they performed so well early this year, while their sensitivity to interest rates explains the rebound seen in November as bond yields dropped.

Corporate Earnings Continue to Boost Returns

Even though economic indicators look increasingly gloomy, the outlook for corporate earnings is still mostly sunny. For the most part, earnings releases for the third quarter of 2023 didn't trigger downward revisions for expected earnings in 2024 (graph 8). However, earnings growth will have to remain robust to justify the rebound in stock market indexes seen in November. Although lower bond yields will help bolster profitability, inflation and sluggish consumer demand are likely to lead to anemic earnings growth or even a decline, capping market gains in 2024.

The S&P/TSX Rally Could Be Short-Lived

Canada's flagship index followed the overall trend in November, bouncing back more than 9% from its October low. But this impressive rally may not last, since the outlook for most sectors in the index is negative. Oil prices fell sharply after peaking in September, along with many other commodities. Earnings in other sectors could also be hit by the coming recession. But an economic recovery and lower yields in the second half of 2024 could send the index bouncing back.

Returns on Risky Assets Will Remain Modest as Central Banks Unwind Their Balance Sheets

The slowdown in global inflation has raised hopes that the rate hike cycle is ending. Like the Fed and the BoC, the European Central Bank will probably start cutting interest rates this spring. But key rate cuts won't prevent central banks from trimming their balance sheets. Excess market liquidity remains well above pre-pandemic levels (graph 9). Unless there's a severe recession and major turmoil in financial markets, we expect central banks to continue shrinking their balance sheets throughout the next year. This, along with the heavy debt loads burdening some governments, could limit the decline in rates over the longer term. The withdrawal of excess liquidity could also be a drag on riskier assets.

The Correlation between Stock and Bond Market Returns May Turn Negative Again in 2024

The negative correlation between equities and bonds, which has long been viewed as a natural hedge for investors with diversified portfolios, went out the window in 2022 and most of 2023. But it looks like liquidity available to the financial system will remain tight in 2024 while the economic outlook will get worse. The trade-off that investors need to make between stocks and bonds could bring back the negative correlation between those two asset classes. This could limit the market rally even if interest rates are cut.