- Jimmy Jean, Vice-President, Chief Economist and Strategist • Hendrix Vachon, Principal Economist

FX Analysis

The US Dollar Is Falling amid More Aggressive Rate Cut Expectations, but Predictions Seem Overblown

August 21, 2024

Highlights

- The US economy has been one of the greatest culprits behind the recent exchange rate volatility. First, the Federal Reserve’s (Fed) statement at the end of July was different from its predecessors: following significant progress toward the inflation target, officials were able to shift their attention to other aspects of the economy. Then the markets reeled after disappointing employment numbers were released on August 2, with the shock wave continuing through the start of the following week.

- The overall result is that the US dollar has depreciated—but there’s more going on than meets the eye. First, the greenback has been penalized by the more aggressive rate cuts now expected by investors. Previously large interest rate spreads between the United States and several other countries have narrowed. The Japanese yen and the euro are among the currencies that have benefited greatly. Meanwhile, other currencies temporarily struggled particularly those in emerging markets and those linked to commodity prices. In addition to interest rate movements, the markets have priced in the effects of a potentially weaker US economy, which is generally bad news for a number of countries and their currencies. Investor risk appetite also dipped temporarily in August, which often leads to increased demand for assets denominated in US dollars and other safe-haven currencies.

- This dip didn’t last long, as evidenced by the recent stock market rally. The prices of several raw materials also recovered. While recession fears have eased, thanks to other data coming from the United States, including strong retail sales, rate cut expectations remain high. Some forecasts are even calling for the Fed to cut interest rates by 50 basis points in September.

- These expectations contrast wildly with the situation in other regions, including in Europe and Japan. Inflation progress has been uneven around the globe. In the eurozone, inflation has been slower to fall, largely due to sticky service costs. As a result, the European Central Bank kept its interest rates unchanged in July after a first rate cut in June. The Bank of England delivered its first interest rate cut in August, but the vote was narrow dashing hopes of multiple rate cuts before the end of the year. And finally, the Bank of Japan (BoJ) announced a second interest rate hike and signalled that additional increases may be necessary. Wage growth is accelerating in Japan, which lends credence to the idea that inflation has durably picked up after decades of threatened deflation. The BoJ will also begin scaling back its asset purchases to normalize its balance sheet.

Main Factors to Watch

- Our interest rate forecasts have slightly changed. We’re now expecting three 25-basis-point cuts in the United States by the end of the year, instead of two. That’s less than the market currently expects. We believe the US dollar could regain some of the ground it has lost, particularly against the euro. The EUR/USD pair could move back around US$1.10 in the coming months. The euro will have an easier time appreciating next year, once the risks of a “hard landing” for the global economy are more convincingly behind us.

- Gains in the yen appear more sustainable, especially since the currency is substantially undervalued on a purchasing power parity External link. basis. The BoJ now seems more seriously committed to raising its interest rates, a move that will be at odds with the Fed and the other major central banks. The USD/JPY currency pair could fall back around ¥140/US$ before the end of the year. This bullish outlook for the yen means that carry trades—borrowing in yen to then buy currencies with higher yields—will become a riskier investment strategy. These popular transactions had amplified the yen’s depreciation in recent years, and reversing the trend could have the opposite effect.

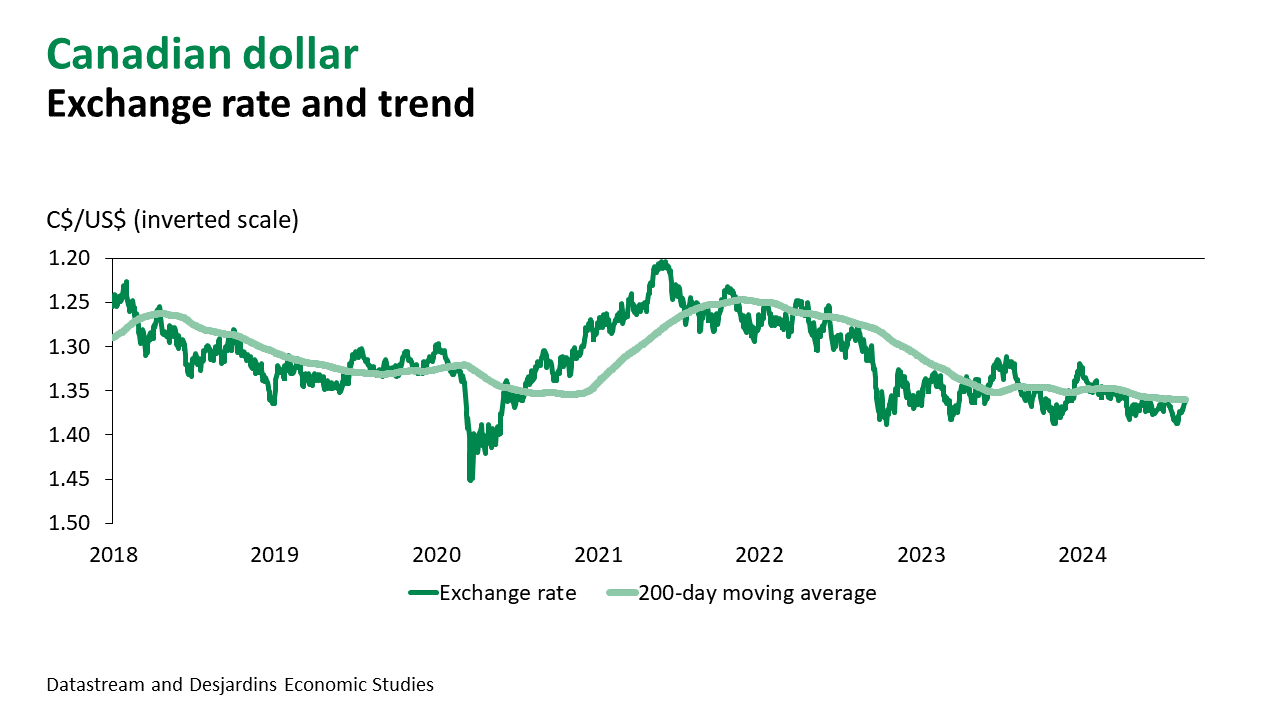

- The Canadian exchange rate is currently close to C$1.36/US$, which is a notable improvement from the start of August, when it approached C$1.39/US$. However, we believe the Canadian dollar will depreciate slightly in the coming months. Investor risk appetite could still waver in the short term, and the Canadian economy seems more fragile. We would be surprised if the Bank of Canada lowered its key rates more slowly than the Fed between now and the end of the year. Given the perceived state of the global economy, we also expect commodity prices to remain volatile.

Main Exchange Rates

Currency Market