- Randall Bartlett

Senior Director of Canadian Economics

Economic News

Canada: Sluggish GDP Suggests the Economy is Going Out as a Zombie for Halloween

October 31, 2023

Highlights

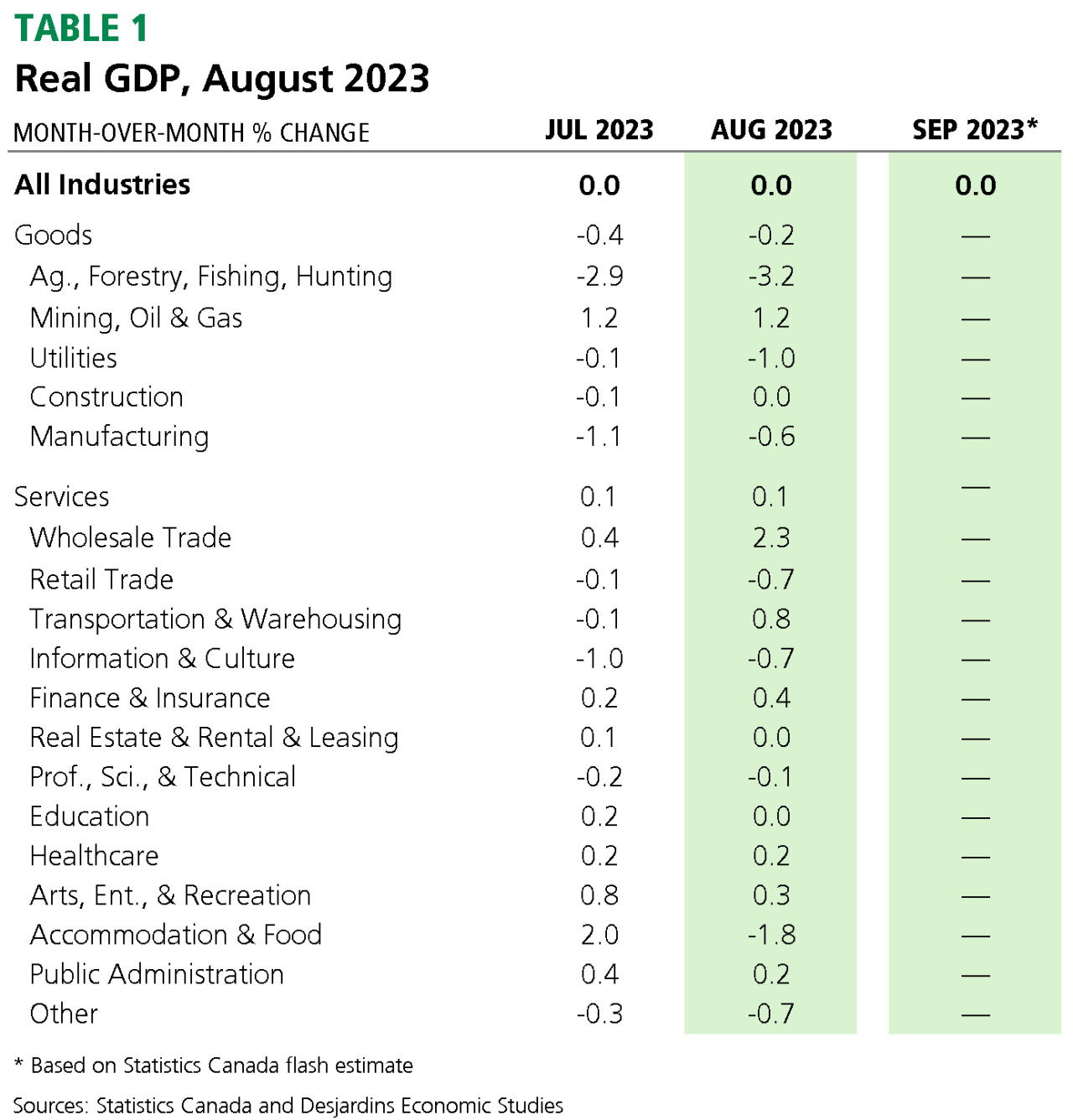

- Real GDP was roughly flat in August, coming in below the consensus of economic forecasters and Statistics Canada’s flash estimate. Services-producing sectors eked out a modest gain (0.1%), while goods-producing sectors contracted in the month (-0.2%). In all, 12 of 20 subsectors posted a decline. See Table 1 for further details.

Implications

While August real GDP surprised to the downside, the broad-based weakness was even more notable. In goods-producing sectors, the only industry to pull off an advance better than a flat print was mining and oil and gas extraction. Otherwise, there was little good news to be found for a third consecutive month. Even in services-producing sectors, the modest headline advance can largely be chalked up to an outsized move in wholesale trade.

Looking ahead, Statistics Canada’s flash estimate for September is pointing to a third consecutive flat print. Assuming it is correct, real GDP by industry would decline at an annualized pace of around -0.1% in Q3 2023. In contrast, we’re tracking growth in real GDP by expenditure closer to +0.1% in the third quarter. Regardless, this suggests real GDP is likely to be unchanged in Q3, well below the Bank of Canada’s recent forecast of 0.8% for Q3 real GDP growth published in its October Monetary Policy Report (MPR).

In addition to tracking 0.1% in Q3, we’re projecting a modest acceleration in growth to around 0.5% annualized in Q4. This is well below where the Bank was in its October MPR but suggests a modestly improved handoff to 2024 than we anticipated when we published our most recent Economic and Financial Outlook External link. This link will open in a new window.. That points to some likely upside to our more downbeat outlook for the Canadian economy next year, albeit not yet enough to throw in the towel on our recession call. As such, we think inflation should come in weaker that the Bank’s upwardly revised forecast, allowing it to remain on hold for the foreseeable future. Indeed, we remain of the view that the next move by the Bank will be a cut around the middle of 2024.