- Randall Bartlett

Senior Director of Canadian Economics

Economic News

Canada: Another Revisions-Driven Wild Ride in the GDP Data

November 30, 2023

Highlights

- Real GDP growth contracted by 1.1% in Q3. This was well below the consensus of economic forecasters (+0.1%) and the Bank of Canada’s forecast (+0.8%). That was offset by a significant upward revision to the second quarter. See Table 1 for more information.

- Monthly real GDP was up 0.1% in September, a tick better than consensus and Statistics Canada’s flash estimate. Statistics Canada expects real GDP by industry advanced by 0.2% in October 2023. Assuming real GDP growth is unchanged in November and December, this would put Q4 growth in real GDP by industry at 1.0% annualized.

Implications

Today’s Q3 GDP release was another shocker. The sharp drop in economic activity was totally unexpected, and in large part reflected downward revisions to monthly data in June through August. The opposite happened to Q2 real GDP growth, where upward revisions to every month from January through May flipped the previous 0.2% annualized decline to a 1.4% increase. Indeed, all of the downward revisions to monthly data at the time of the last quarterly GDP release were almost entirely reversed. The frequent and substantial revisions to these key economic data are making their interpretation difficult.

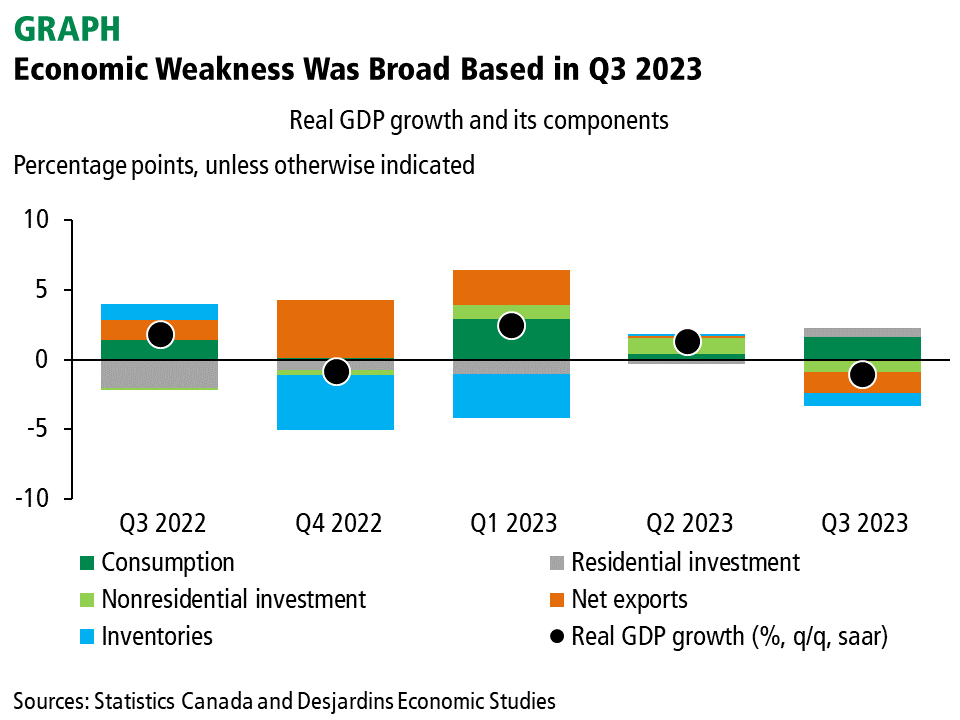

Unpacking the release, it’s clear the Canadian economy experienced broad-based weakness in Q3 (graph). Business investment contracted sharply on an aggressive reversal in fortune for investment in machinery and equipment. Net exports dropped on falling demand for Canadian goods and services. And household spending remained essentially flat for the second consecutive quarter. At the same time, the pace of growth in compensation of employees slowed markedly from Q2. Despite this, the savings rate inched higher as disposable income growth outpaced the advance in consumption.

Looking ahead, the positive monthly real GDP data for September and October point to an acceleration in growth in the final quarter of the year. We’re currently tracking annualized real GDP growth in the range of 0.5% to 1% for the fourth quarter of 2023, in line with the 0.8% pace expected by the Bank of Canada in its October 2023 Monetary Policy Report.

Along with a weakening labour market and the slowing pace of underlying inflation, today’s GDP data should keep the Bank on the sidelines for the foreseeable future. Indeed, we believe the next move by the Bank will be a cut in Q2 2024. That said, the Bank is likely to use next week’s press release to recognize recent progress but reiterate it remains prepared to do whatever is necessary to ensure inflation returns to its 2% target.