- Randall Bartlett

Senior Director of Canadian Economics

Economic News

Canada: Q1 GDP Points to Rate Cuts Just around the Corner

May 31, 2024

Highlights

- Real GDP growth advanced by 1.7% annualized in Q1 2024. This was less than the consensus of economic forecasters (2.2%) and well below the Bank of Canada’s more upbeat outlook (2.8%). Real GDP growth in Q4 2023 was revised lower as well (to 0.1% from 1.0%). Table 1 provides more details on the release.

- Monthly real GDP was flat in March, in line with consensus and Statistics Canada’s flash estimate. Statistics Canada expects real GDP by industry to advance by 0.3% in April 2024. Assuming real GDP is unchanged in May and June, this would put Q2 2024 growth in real GDP by industry at 1.5% annualized.

Implications

The softer-than-expected print for Q1 2024 real GDP growth should be music to the ears of Canadians looking for the Bank of Canada to begin cutting rates soon. But the details of the release were more positive than the headline suggests. Consumption was particularly strong (graph 1), as household spending on services posted another solid quarterly advance. But this still wasn’t enough to keep pace with income growth, leading to a further increase in the household savings rate. Business investment also made a notable comeback after a dismal end to 2023, despite a substantial decline in corporate profits in the quarter. Even trade defied the monthly data published throughout the first quarter, eking out a marginal advance. It was only inventories that acted as a drag on headline growth in Q1.

Looking ahead, the solid monthly real GDP data for April point to another positive print in the second quarter of 2024. We’re currently tracking annualized real GDP growth in the range of 1.5% to 2% in Q2, broadly in line with that forecast by the Bank of Canada in its April 2024 Monetary Policy Report (graph 2). But when combined with the downward revision to Q4 2023 and weaker-than-expected Q1 2024, it seems likely that the Bank will adjust down its outlook for 2024 real GDP growth when it publishes its next forecast in July.

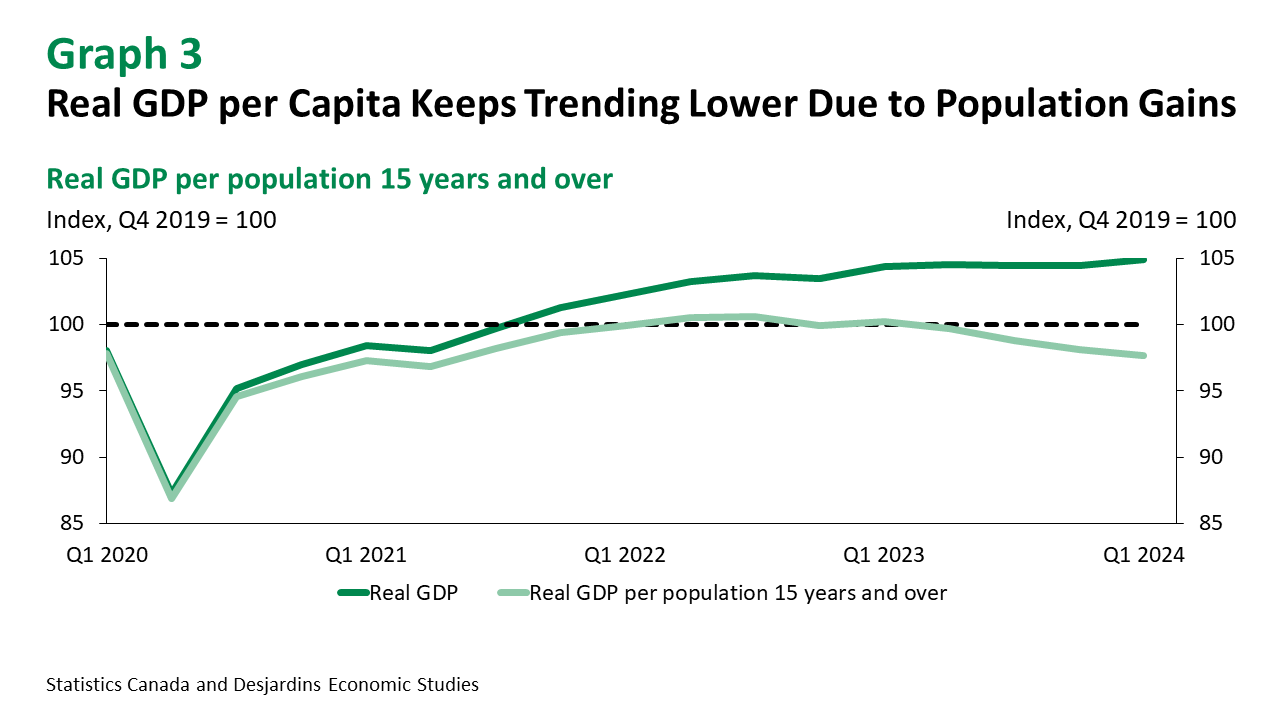

While headline real GDP growth looks as though it will be respectable in the first half of this year, it will be notably below the pace recently forecasted by the Bank of Canada. It will be even weaker on a per capita basis (graph 3). The labour market has also showed some signs of cooling, with the unemployment rate edging higher as employment gains fall short of population growth. Inflation is coming in softer than the Bank expected as well. All these indicators weigh heavily into the Bank of Canada’s decisions on the direction of interest rates. As such, when combined with still weak survey data and elevated business bankruptcies, we remain of the view that the Bank is likely to begin cutting interest rates at its upcoming June meeting.