- Randall Bartlett, Senior Director of Canadian Economics • LJ Valencia, Economic Analyst

Economic News

Canada: GDP Beat the BoC’s Forecast, But It’s Not Likely to Happen Again in Q3

August 30, 2024

Highlights

- Real GDP growth advanced at an annualized pace of 2.1% in Q2 2024. This beat the consensus of economic forecasters (1.8%) and was above the Bank of Canada’s (BoC) more downbeat outlook (1.5%). Real GDP growth in Q1 2024 was revised up a tick as well (to 1.8%). Table 1 provides more details on the release.

- Monthly real GDP was flat in June (0.0%), slightly below consensus and Statistics Canada’s flash estimate (at 0.1%, respectively). Statistics Canada expects real GDP by industry to be unchanged in July 2024 as well. Assuming real GDP growth is unchanged in August and September, this would put Q3 2024 growth in real GDP by industry at 0.1% annualized.

Implications

Another quarter, another respectable print for Canadian real GDP growth. But take a look under the hood, and Canada’s growth engine looks to be sputtering. First, interest-rate sensitive sectors like durable goods consumption and residential investment both contracted in Q2. Indeed, if it weren’t for services consumption, which also slowed relative to Q1, household purchases wouldn’t have advanced in the quarter. And while business investment was positive, most of that is owing to higher spending on aircraft and ships, which corresponded to an increase in imports of those same goods in the quarter. When combined with a decline in export volumes, net exports were a drag on growth in Q2. Meanwhile, government consumption and investment contributed 1.7 percentage points to growth in the second quarter, meaning private activity was in the doldrums—never a good sign (graph 1). And much of the increase in government spending related to stronger compensation for public servants, which is not necessarily a sign of economic strength. In better news, corporate profits clawed back some of the losses in the first quarter thanks in large part to the oil and gas extraction sector. Compensation of employees also made a solid advance, helping to push the saving rate higher. At 7.2%, it reached its highest level since 1996 outside of the pandemic.

Looking ahead, despite no growth in June and an outlook for a flat print in July, we’re currently tracking annualized real GDP growth in the range of 1.0% and 1.5% in Q3. This is well below the 2.8% forecast by the BoC in its July 2024 Monetary Policy Report (graph 2). The BoC’s optimistic outlook for Q3 seems to be partly predicated on TMX providing a tailwind to growth, although our research External link. suggests that may be overstated. The BoC’s expected rebound in auto production also seems to be wishful thinking if the Ward’s production forecast is any indication, and may ultimately provide more of a tailwind to the final quarter of 2024.

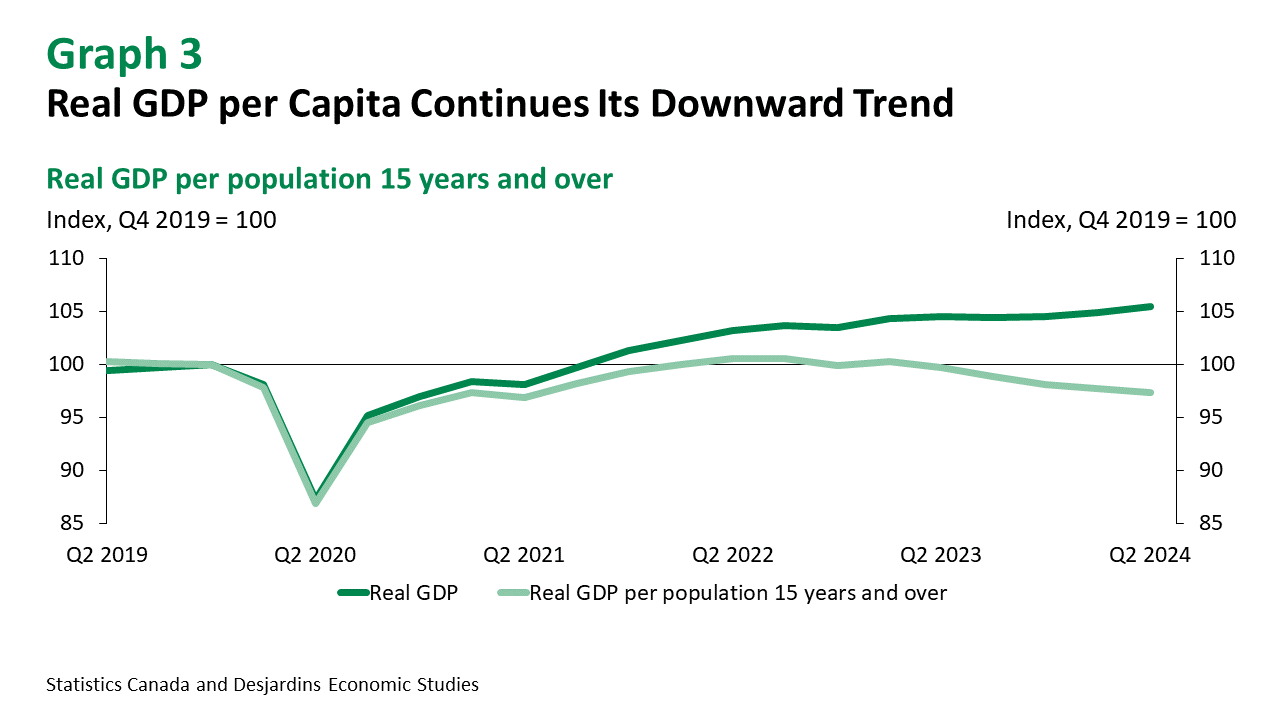

Despite better-than-expected growth in Q2, our GDP tracking suggests there may be more slack in the economy when the dust settles on the third quarter than the BoC was expecting in July. It will be even weaker on a per capita basis (graph 3). The labour market is also showing signs of cooling, with the unemployment rate edging higher as employment gains fall short of population growth. Inflation is coming in softer than the BoC expected as well. All of these indicators point to another 25 basis point cut at next week’s interest rate announcement. Similar sized cuts at each of October and December meetings are also expected. The growing debate should be whether the BoC might need to cut rates by more than 25 basis points at one of these meetings. We expect a dovish BoC next week. And depending on its tone, the risks tilt towards markets pricing in the possibility of a larger cut than they are currently.