- Kari Norman

Economist

Economic News

Canada: Home Sales Fall, but Restoring Affordability Remains a Long Way Away

May 15, 2024

Highlights

- The pace of housing starts in Canada held steady in April at 240k (saar), with continued slight weakening in multi-unit housing construction offset by marginal growth in single-family housing. Table 1 below summarizes key data points.

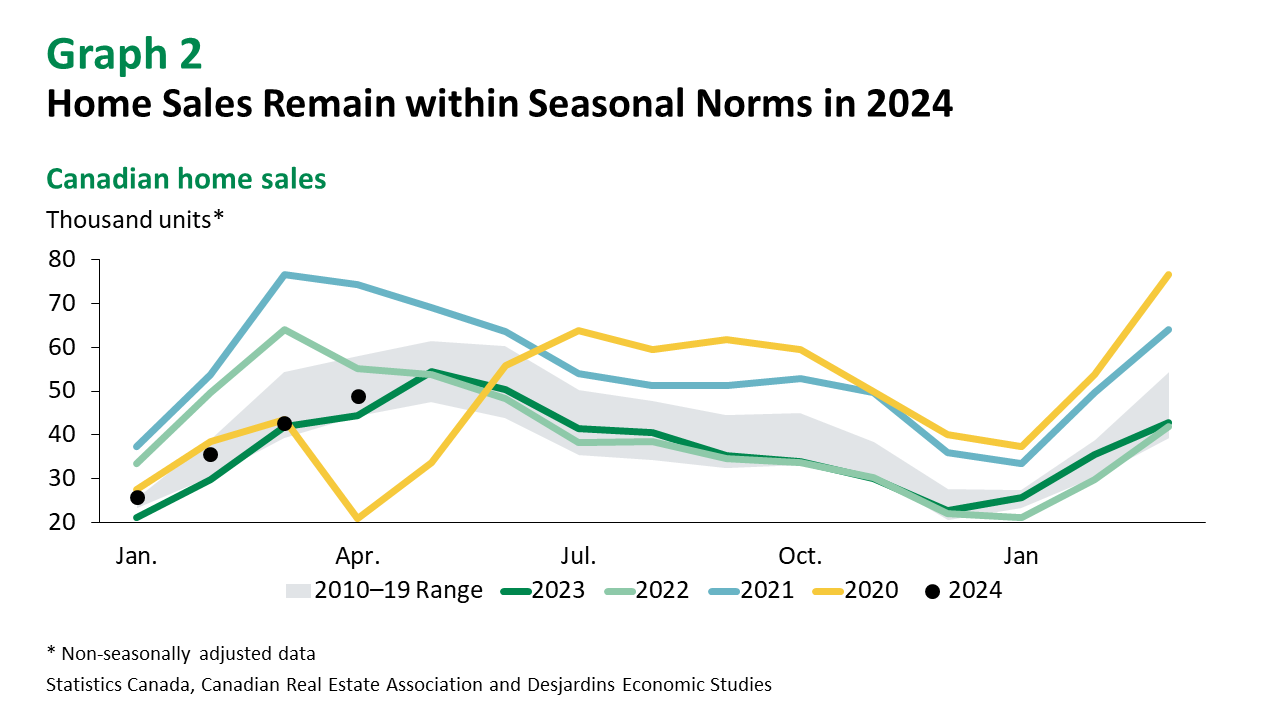

- Home sales in Canada fell by 1.7% in April. Table 2 below summarizes key data points.

- Early in Q2, our tracking suggests real annualized GDP growth of near 1.7% in the quarter. This is slightly above the Bank of Canada’s (BoC) estimate published in April. We’re still tracking an advance just above 2% for Q1, which is below the latest BoC projection of a 2.8% gain.

Implications

The outlook for home construction appears to be weakening in and around Toronto. A recent report External link. by Urbanation highlighted that new condo presales in Q1 (1,461 units) were at levels not seen since early 2009 and the late 1990s—periods where the region’s population was significantly lower. Projects in preconstruction were averaging 50% presold, well below typical construction financing requirements of 70% absorption. Recent government spending commitments will take time to work their way through the system before shovels break ground. Homebuilder sentiment also continues to be gloomy in both single- and multi-family housing—unsurprising, given recent news reports of construction projects being paused or cancelled. The effects of high interest rates may have caught up to the condo construction market. It remains to be seen how quickly this effect will unwind once interest rates start to come down.

The single-unit residential construction market isn’t faring much better. Starts grew marginally in April, but remain down more than 40% from the peak in early 2021 (graph 1).

Regionally, as compared to March there were more shovels breaking ground in Ontario and Alberta, offset by weakening in BC and Quebec. That said, starts are trending lower in Canada’s largest province, where many projects last year were financed before interest rates increased.

Existing home sales remain within seasonal norms, albeit close to the lower end of the range (graph 2). National average and benchmark prices remained steady in April. Decades-high population growth, resilient job creation, and solid wage gains are likely putting a floor under prices, even as still-high mortgage rates keep buyers on the sidelines for a while longer. Despite the softer home sales in April, average national sale prices remain firm. They were up about 1% over the previous month and approaching 5% over April 2023.

Regional housing market differences persisted in April. Supply-demand conditions in Vancouver and Toronto are once again trending more in favour of buyers. By contrast, Calgary and Halifax are firmly in sellers’ market territory.

Looking through the remainder of 2024, the gradual unwinding of interest rate hikes expected to begin this June may bring some buyers back to the market. But given the pickup in home sales following the pause in monetary policy tightening in early 2023, the BoC will be watching carefully to avoid a repeat this year. Residential construction will continue to be buffeted by challenges such as labour shortages in the trades, inflation in building materials costs and weaker homebuilder sentiment. That said, the recently announced plan by the federal government to reduce non‑permanent resident admissions should help bring overall housing demand more in line with supply over time.