- Marc Desormeaux

Principal Economist

Economic News

Canada: New Cracks Emerge in the Housing Market Foundation as Rate Hikes Resume

July 14, 2023

Highlights

- Existing homes sales rose by a modest 1.5% in June on a seasonally-adjusted basis, a fifth consecutive increase that followed advances of 11.1% and 4.6% in April and May, respectively. Home purchases were 4.7% above June 2022 levels.

- Sales were up in about half of local markets in June, in contrast to 70% in May. Greater Toronto saw its steepest drop (-6.9%) since September of last year, while Vancouver also recorded a loss in the month (graph 1). In Ottawa and the province of Quebec, sales were largely unchanged following healthy gains in May, while purchases remained healthy in the prairies and Halifax.

- The average sale price of an existing home fell by 0.7% to $709K in June—the first decline in five months—to sit 6.7% above the same month in 2022. Despite that, it now sits about 10% below the February 2022 peak, having recovered more than half the ground lost through January of this year.

- The composite benchmark price, which accounts for market composition of sales activity, rose by 2% in June, a third successive monthly increase following 12 declines in a row. Still, it was 4.5% lower than year-earlier levels.

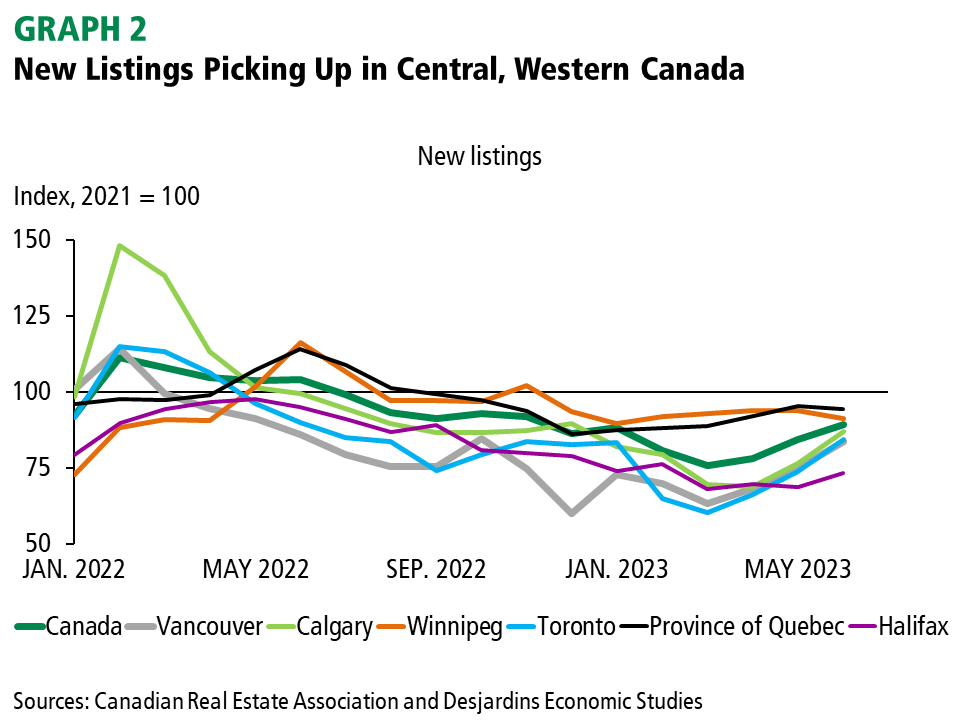

- The number of new listings rose for the third consecutive month, outstripping home purchases with a 5.9% climb. While that lowered the sales-to-new listings ratio to 63.6% in June, it was a fourth straight month in sellers’ market territory.

- There were 3.1 months of inventory available at the national level in June. That was unchanged from the prior month, but nonetheless lower than any level recorded prior to 2020. Ontario was the only province to experience an increase in this respect.

Though home sales certainly did not slow as significantly as we feared, many prospective buyers look to have responded to the Bank of Canada’s decision to resume interest rate hikes in June. The slowdown in home sales momentum was reasonably broad-based, with notable drops in high-priced Toronto and Vancouver, which had been on a tear for several months.

The continued climb in new listings (graph 2)—prior weakness in which contributed to price gains earlier this year—is a development that must be monitored closely. Whether it reflects investors trying to time the market in an environment of strengthening prices or the response of some mortgage holders to sharply higher debt servicing costs will only become clearer in the next few months. Still, most local markets remain tight even after some rebalancing of demand-supply conditions in June. But if the recent listings trends persist amid higher interest rates and softening resale activity, that presents clear downside risk to Canadian home prices.

Implications

Halfway through 2023, many of Canada’s local housing markets have recorded solid gains, but the trend doesn’t look to be their friend. A second interest rate increase earlier this week—following the pause that began in January—will put further upward pressure on mortgage costs. That suggests a further softening of sales activity in the coming months, particularly in expensive markets within Ontario and BC. Those cities were hardest hit when monetary tightening began and have also seen the steepest increases in mortgage payments since the start of the pandemic (graph 3). The prairies still face better prospects given their advantage with respect to affordability.

While we do foresee some cooling of the recent surge in resale activity in the coming quarters, we also expect new housing supply to ease, putting a floor under prices. Home construction did not weaken as much as could have been expected during the recent period of higher interest rates. But if history is any guide, that can’t last, particularly if economic growth slows, financing costs are high, and resale activity remains well below its recent peak. And of course, population growth continues to run at multi-decade highs, complicating the challenge of delivering a sufficient level of affordable housing to prospective homebuyers.

Comments