- Marc Desormeaux

Principal Economist

Economic News

Canada: Rising Unemployment Rate Supports Another Rate Cut in July

June 7, 2024

Highlights

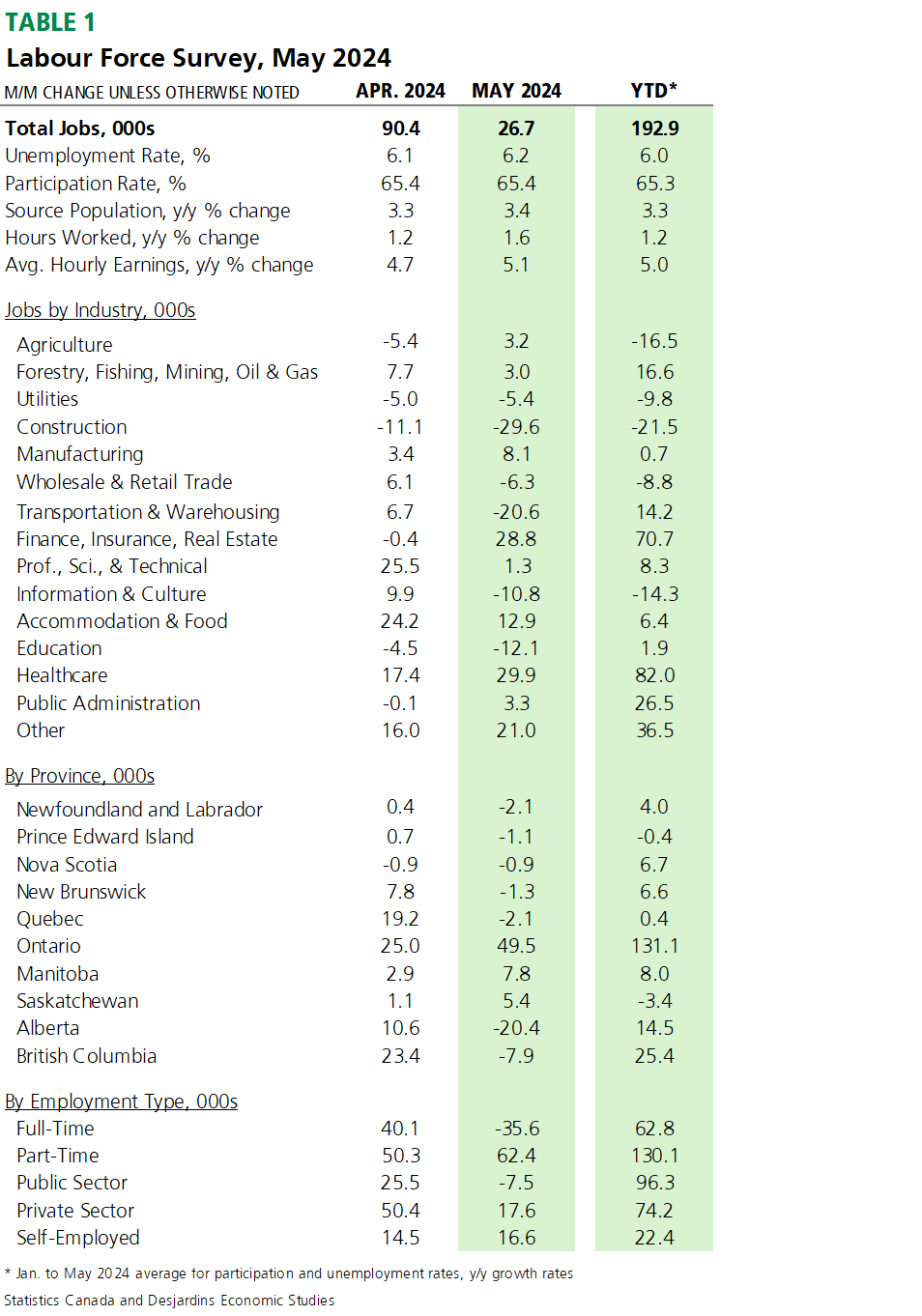

- Total Canadian employment increased by 27k in May 2024, while the unemployment rate rose a tick to 6.2% to continue the upward trend seen since mid-2022. Table 1 summarizes key data points.

- The data brings our tracking of Q2 2024 real annualized Canadian GDP growth to about 1.8%, a touch higher than the last Bank of Canada (BoC) estimate published in April.

Implications

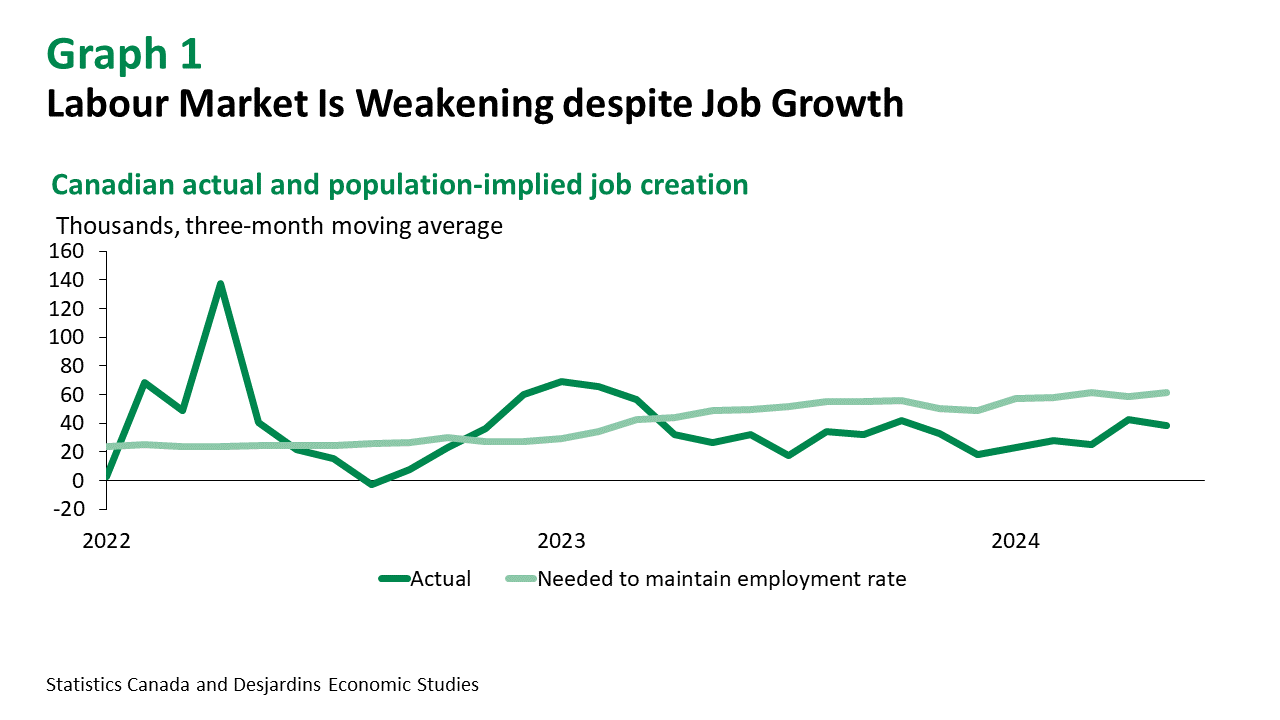

The headline numbers were mostly soft. While the economy continued to churn out jobs, monthly gains in hours worked eased and full-time positions experienced their largest one-month drop in almost two years. Canada’s employment rate also fell to its lowest level since late 2021. The data continue the trend of job creation being weaker than what’s been needed to keep the employment rate steady because of the decades-high population growth (graph 1). We’ve highlighted this many times before as a sign that the labour market is softening and the Bank of Canada noted this point in Wednesday’s rate cut announcement External link..

Still-torrid population gains continue to be a mixed bag for Canada’s economy and inflation outlook. They remain a tailwind for economic activity, which could potentially slow the pace of disinflation, especially in an environment of limited housing supply. But they’ve also helped fill job vacancies and kept a lid on wage pressures. Ottawa’s plan to lower the temporary resident population External link. by 20% should reduce the primary driver of recent demographic gains later in 2024 and beyond.

Although Ontario witnessed the strongest job gains of any province last month, its labour market has arguably built up the most slack since the start of last year (graph 2). Rises in BC’s unemployment rate have also generally outpaced the national average over that span, in line with our view—detailed in the latest Desjardins Provincial Outlook External link.—that the most interest rate-sensitive provincial economies will feel the coming economic slowdown most.

May’s pickup in wage growth is less positive from the perspective of controlling price pressures, but there are additional points to consider. The central bank noted this week that it was continuing to watch wage gains (despite signs of gradual progress towards stabilization). However, the BoC looks to a broad group of wage indicators when making decisions on the direction of monetary policy, most of which show a more contained pace of compensation gains. Moreover, the fact that corporate profits registered a fifth consecutive year-over-year decline in Q1 suggests that higher wage costs are not being transmitted fully into consumer prices.

Ultimately, May jobs’ data don’t change our view that the BoC will reduce its policy rate again in July. Although wage pressures remain a risk to watch, the labour market is still softening and inflation is easing. The Bank should—for now—take comfort in these trends.