- Marc Desormeaux

Principal Economist

Economic News

Canada: Job Gains Still Lagging Population Growth as We Kick Off 2024

February 9, 2024

Highlights

- Net total Canadian employment rose by a solid 37k in January 2024. The unemployment rate fell to 5.7%, its first decline in over a year. Table 1 summarizes key data points.

- There was not much change in our Q1 2024 tracking, which still suggests real annualized GDP growth could best the gain last forecast by the Bank of Canada.

Implications

2024 is shaping up to be a year of rematches: the 49ers versus the Chiefs for the Super Bowl, Joe Biden versus Donald Trump for the US presidency, and according to today's data, hefty population and wage gains versus the Bank of Canada's 2% inflation target.

First off, Canada’s labour market reported mixed results despite the headline jobs gain and increases in hours worked. Notably, full-time employment fell for the second consecutive month in January. Private sector hiring also lagged that of the public sector, continuing the trend seen in much of the past year.

More importantly, as we’ve highlighted many times before, hiring numbers alone can be misleading given the surge in population growth. Even after a nearly 40k gain in January, job creation continued to significantly lag the rate needed to maintain the employment rate to start the year (graph 1). As such, the labour market is still softening despite higher numbers of net new positions.

We had been seeing signs that population growth was slowing, but it appeared to jump back up again in January. That suggests that a softening labour market is not yet translating into weaker demand for temporary labour—the principal driver of the recent population growth spurt External link.—a trend our latest projections External link. assumed would continue in 2024. But we’ll have to wait a few months for confirmation. The recent cap on international students won’t show up in the population numbers until later in the year, and even then, the impact will be modest.

These hefty population gains continue to have mixed implications. They present an upside risk to inflation in the short run and could also hurt housing affordability in an environment of significant supply shortfalls. Our latest forecasts do not anticipate a return to pre-pandemic affordability levels in the next two years External link.. But given significant improvements in newcomer labour market outcomes in recent years, there’s a clear argument that these individuals can help fill job shortages, increase the supply of available workers and reduce potential wage-push inflation over time.

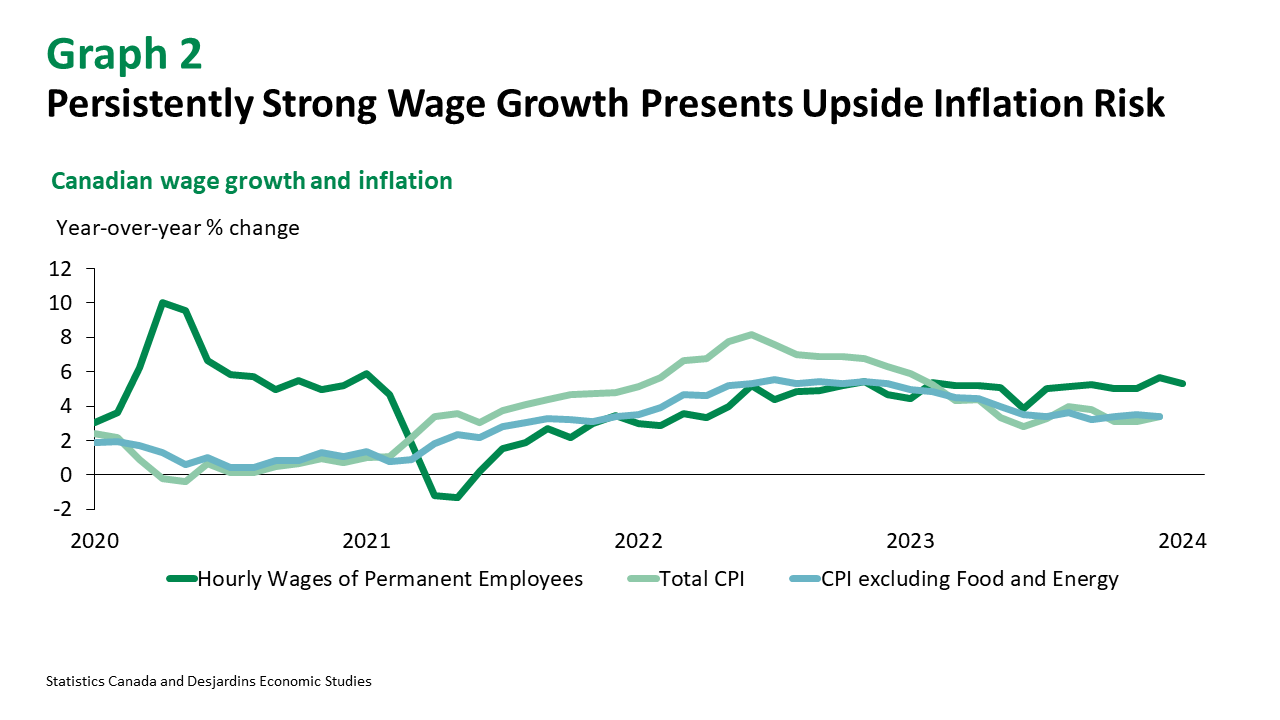

January’s still-strong year-over-year wage gains (graph 2) are less positive for inflation-control efforts. The Bank of Canada (BoC) tracks permanent employees’ wages closely to measure signs of possible wage-push inflation. While the year-over-year increase was more modest in January than it was in December, it still underscores the risk of wage stickiness, which the BoC highlighted in its recent rate announcement and will continue to monitor closely.

For now, we’re sticking to our call that the Bank of Canada will begin reducing its policy rate in the second quarter of 2024. We suspect that the central bank will put more weight on slowing economic activity, easing price pressures and falling job vacancies. And we’re still of the view that as Canadian consumers and businesses increasingly feel the full effects of prior increases in borrowing costs, it will prompt a less restrictive monetary policy stance. But as we begin the new year, there’s no question that high population and wage growth still present upside risks to inflation.