- Randall Bartlett

Senior Director of Canadian Economics

Economic News

Canada: Inflation Accelerates in August but Should Trend Lower from Here

September 19, 2023

Highlights

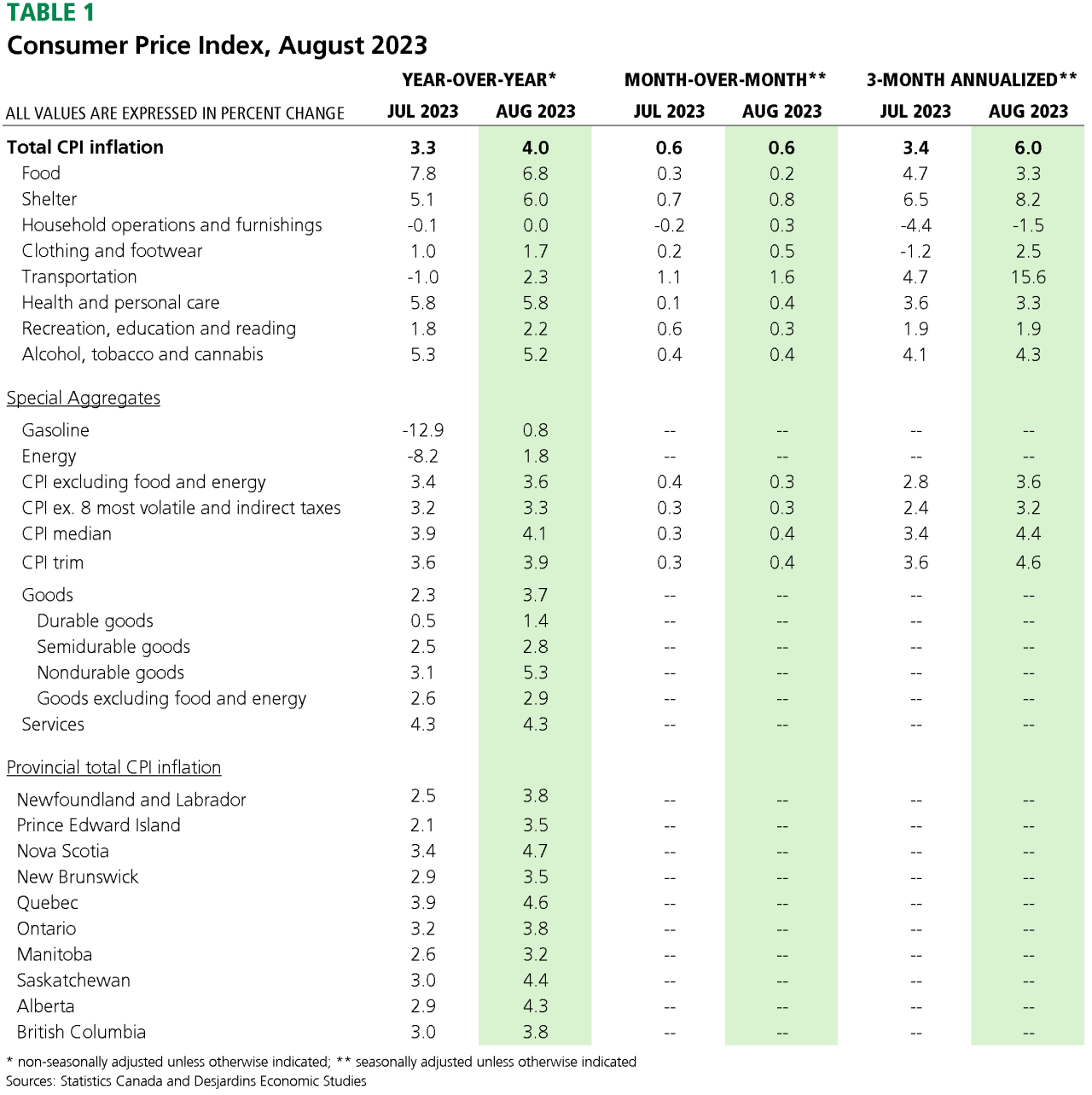

- Headline CPI accelerated sharply to 4.0% y/y in August over the same month last year, beating economists’ expectations for a 3.8% move. Meanwhile, monthly price growth advanced by 0.6% m/m on a seasonally-adjusted basis, in line with the pace it clocked in at in July. Table 1 summarizes the key data points.

Implications

As was widely anticipated, headline CPI inflation reaccelerated in August, albeit coming in hotter than economists expected. At 4.0% y/y, it is now more than a percentage point higher than the 2.8% in June, which was the slowest pace of year-over-year price growth since March 2021.

There are reasons for concern in the August inflation print besides the headline number. Most of the major CPI categories saw a reacceleration in price growth even after removing the impact of seasonality. And while some of this can be chalked up to a jump in energy prices, month-over-month changes in a broad suite of underlying inflation measures also advanced in the month.

Digging more deeply into the data, the August inflation data looks even worse. The Bank’s preferred measures of core inflation—CPI median and trimmed mean—reaccelerated to 4.1% and 3.9%, respectively. Turning to the 3-month annualized change in these measures, each jumped a full percentage point to a respective 4.4% and 4.6% in August. This is the fastest pace of near-term core price growth since April of this year. On a slightly more positive note, the central bank’s latest measure of core inflation—core services excluding shelter—decelerated to 4.1%, from 4.3%.

August’s headline inflation print stands in contrast to the relatively weak macroeconomic data in Canada. The Bank of Canada recognized as much in the press release that accompanied its latest rate announcement, pointing to “… recent evidence that excess demand in the economy is easing …” This followed a 0.2% annualized contraction in Q2 real GDP, well below the Bank’s forecast of 1.5% published in the July 2023 Monetary Policy Report. We’re now tracking real GDP growth of around 0.3% annualized in Q3, similarly below the Bank’s most recent projection.

Further, the jump in August inflation was partly the result of higher gasoline prices and base effects, both of which are expected to subside somewhat in September. As such, we think inflation should trend lower from here, supporting the Bank’s decision to stay on hold earlier this month. Markets have moved to price in a 50% chance that the BoC resumes hiking at its next meeting in October. By then, it will have collected more data on growth and employment, as well as another inflation print. Those will help determine whether a hike becomes warranted. But for now, our forecast remains consistent with the BoC leaving rates on hold until Q1 2024.