- Randall Bartlett

Senior Director of Canadian Economics

Economic News

Canada: Slower Inflation in June All but Guarantees a July Rate Cut

July 16, 2024

Highlights

- Headline CPI rose 2.7% y/y in June, down two ticks from May. Prices fell 0.1% m/m, two ticks lower than the consensus forecast. Table 1 summarizes the key data points.

Implications

Canadians can breathe a collective sigh of relief after today’s release of the June CPI data. With headline inflation coming in below last month’s print, May’s reacceleration in price growth looks like it may have been an aberration in an otherwise good run of data in the first half of 2024.

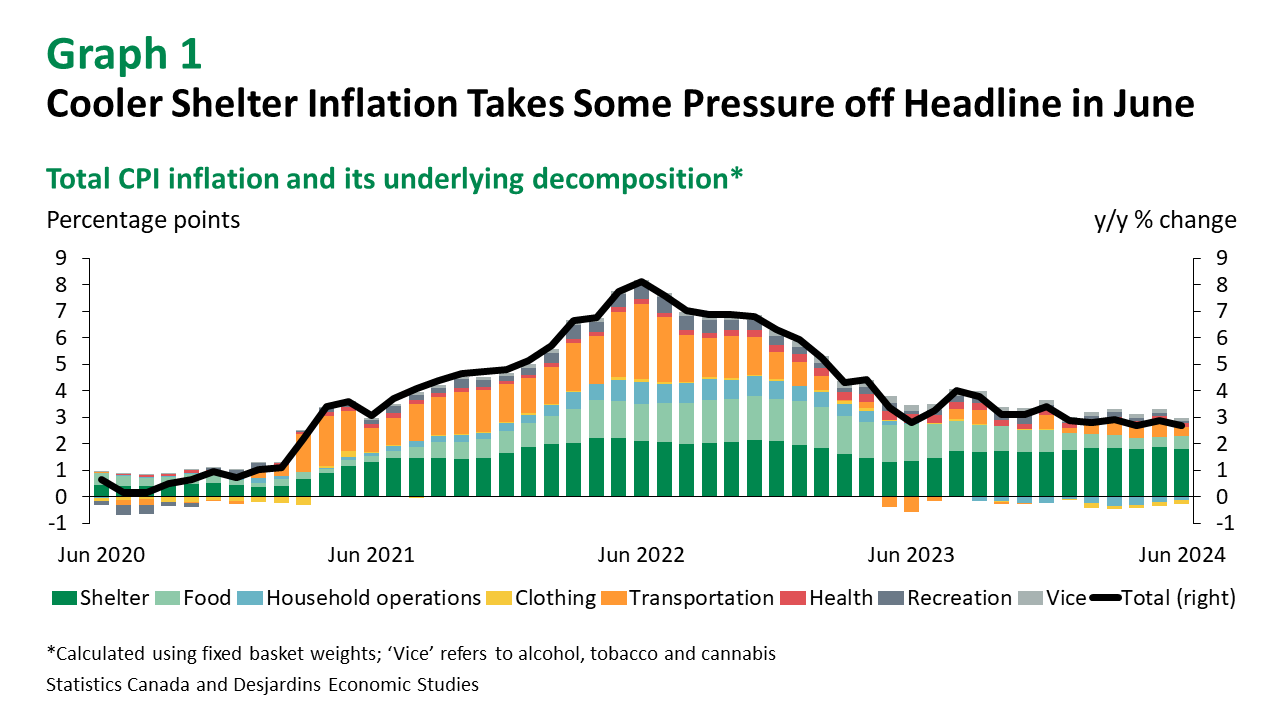

Digging into the details of the June release, the softer inflation print was relatively broad based. On a year-over-year basis, all but food among the main aggregate categories slowed over the prior month. Shelter price gains slowed again (6.2%), thanks largely to a slower pace of price gains in utilities (1.6%). However, shelter remains the single biggest contributor to headline inflation (graph 1). Energy played a particularly important role in June, just 0.5% y/y higher than a year ago thanks to a second consecutive monthly decline. But on a less positive note, inflation excluding food and energy was up 2.9% from last year, matching the May move which bucked the trend deceleration that started in early 2023.

Looking to underlying inflation, the Bank of Canada’s preferred measures of core year-over-year price growth—CPI median and trimmed mean—were essentially unchanged in June (averaging 2.8% y/y), managing to stay under 3% for the third consecutive month. But on a 3-month annualized basis, these measures accelerated for the third month in a row, hitting a five-month high of 2.9% respectively (graph 2). Meanwhile, the more universally referenced total CPI inflation excluding food and energy inflation held steady at 3.0% in June on a 3-month annualized basis—the second time this year that this indicator had a 3-handle. In better news, the Bank’s former preferred measure of core inflation—CPIX (CPI excluding the 8 most volatile components & indirect taxes)—was unchanged at a much more modest 2.1% on a 3-month annualized basis.

With the slowing price growth in June, headline inflation has now remained within the Bank of Canada’s 1% to 3% target range for six consecutive months. At 2.7% y/y, headline inflation in Q2 2024 was below the Bank’s forecast of 2.9% in the April 2024 Monetary Policy Report. And despite accelerating recently, most measures of underlying inflation remain below 3% as well and have been for a few months. At the same time, the Bank of Canada’s latest consumer External link. and business External link. surveys showed inflation expectations continuing to return to earth in Q2 2024. Add to that Q2 real GDP growth, which is tracking roughly in line with the Bank’s most recent forecast (see our latest Economic and Financial Outlook External link. for more information). Taken together, the June inflation print is just the latest indicator to reinforce our call for a cut at next week’s Bank of Canada rate announcement.