- Royce Mendes

Managing Director and Head of Macro Strategy

Economic News

Canada: More Core Disinflationary Pressures in March

April 16, 2024

Highlights

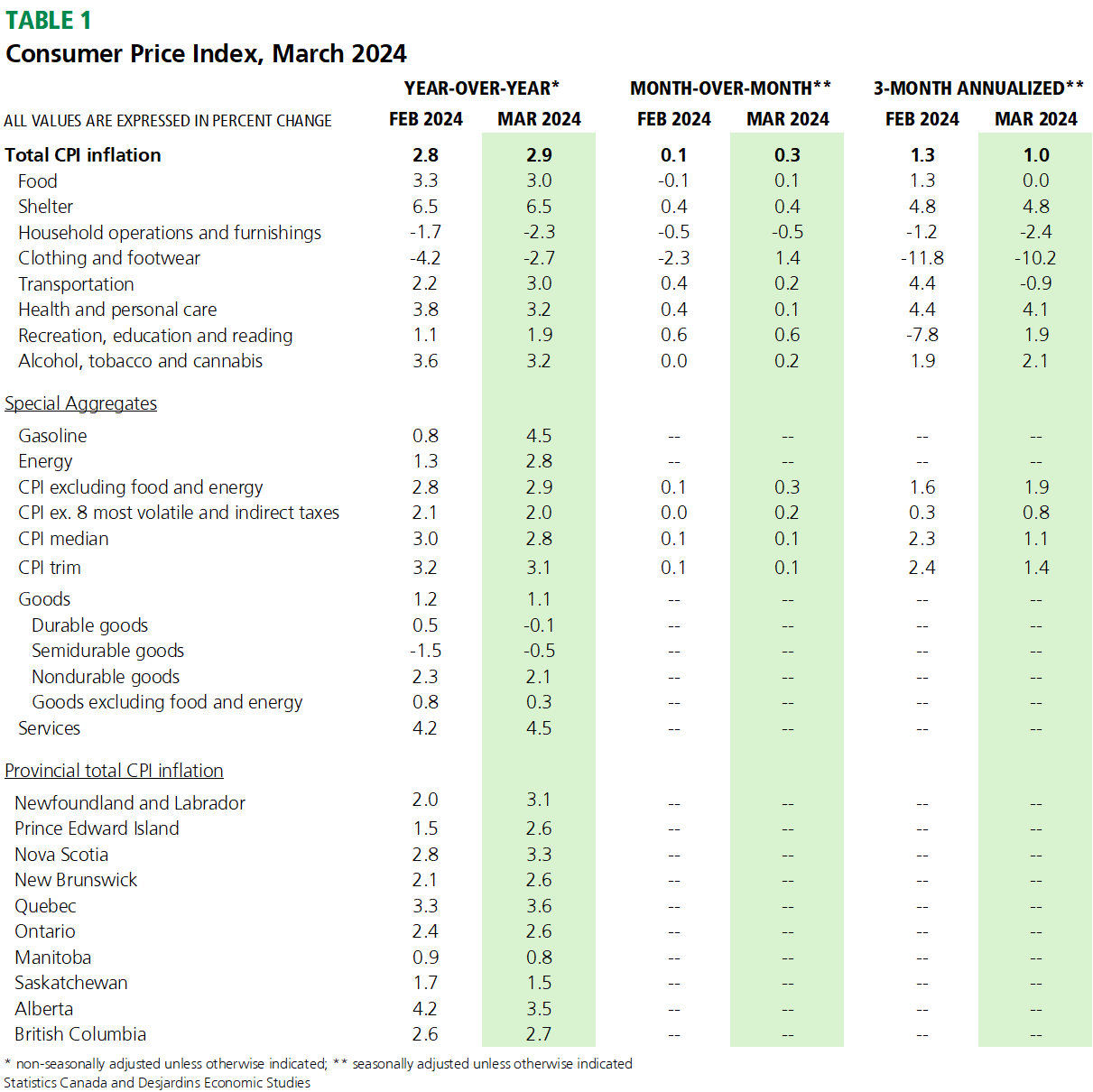

- Headline CPI rose 2.9% y/y in March, in line with economists’ expectations. Prices rose 0.6% m/m, but only 0.3% after adjusting for seasonal effects. Table 1 summarizes the key data points.

Implications

Bank of Canada Governor Tiff Macklem got exactly what he was hoping for in the latest CPI release. Despite a slight increase in headline and ex-food and energy inflation, a host of other metrics tracking underlying pressures point to a further normalization in consumer price growth.

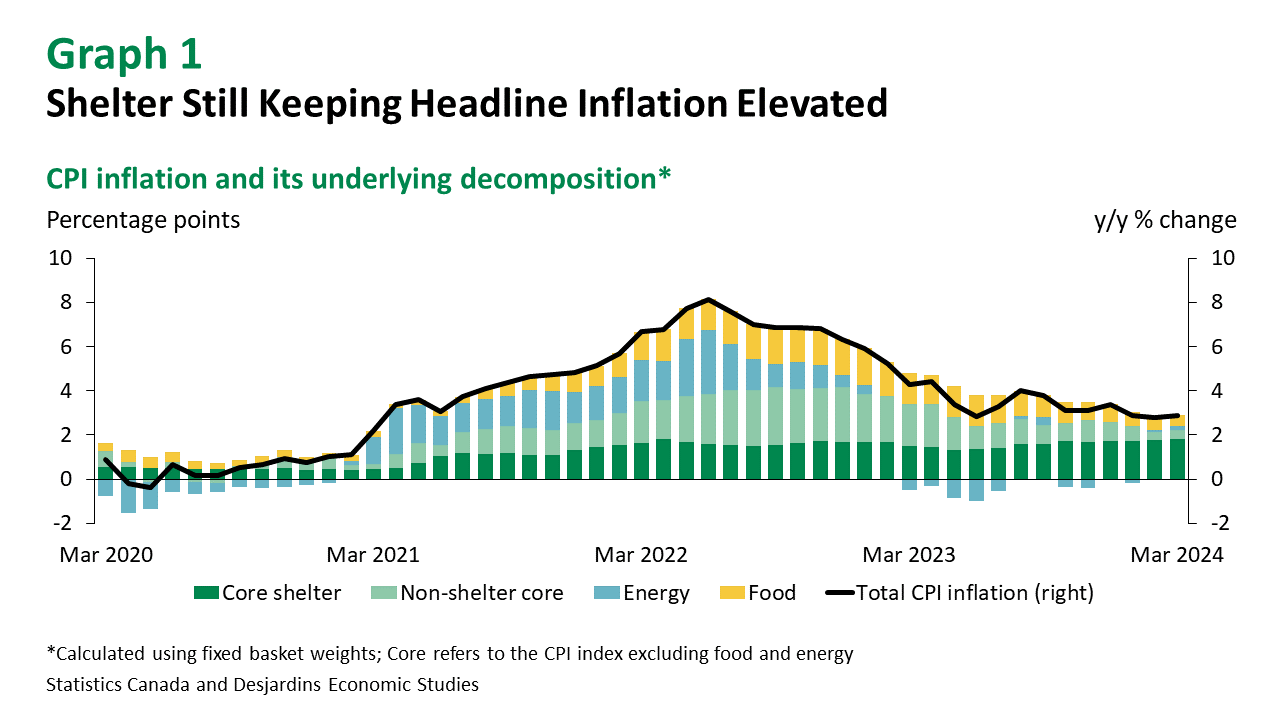

Shelter remains the single most important contributor to total inflation (Graph 1). Excluding shelter, inflation is tracking just 1.5% and has been below the central bank’s 2% target for most of the past six months. High and rising shelter costs, coupled with the recent increase in gasoline prices, appears to be eating away at consumer finances. That’s seeing many businesses finding it more difficult to raise prices as quickly or as frequently as they were in recent years.

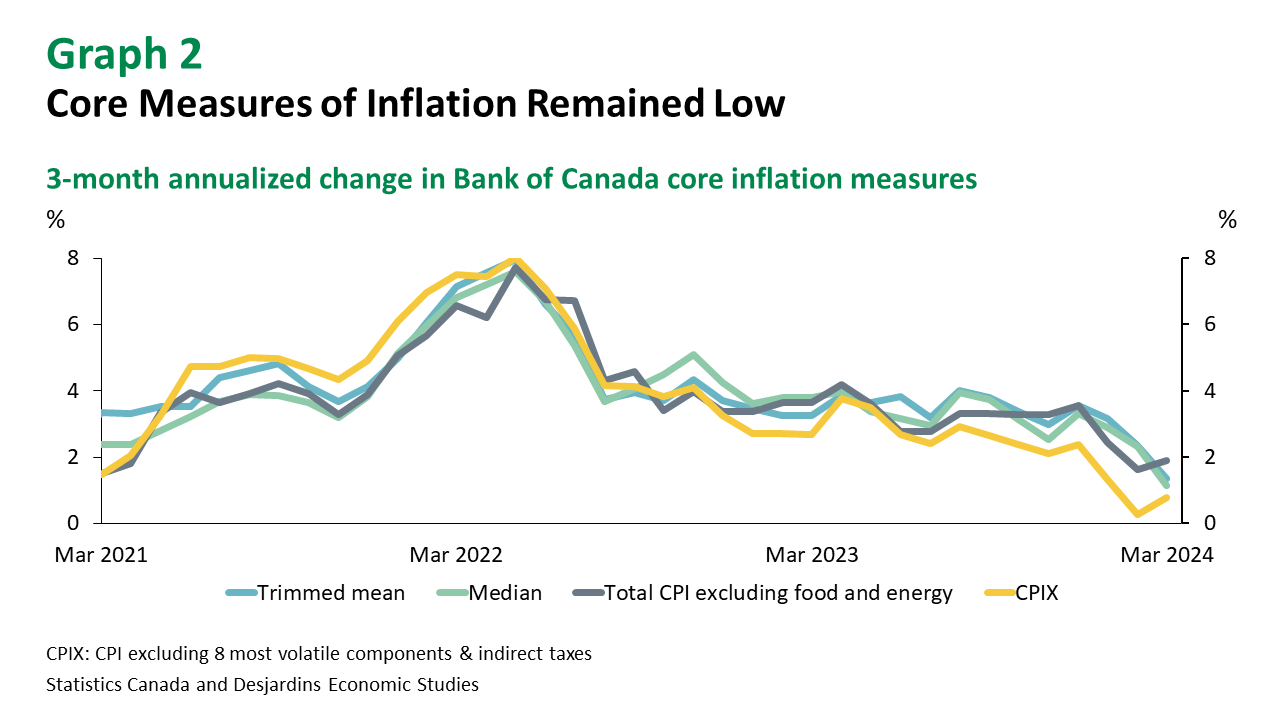

All this plays into the Bank of Canada’s hands. Total inflation matched the central bank’s forecast for the first quarter of the year and consumer prices could undershoot the projection for the second quarter. Moreover, the Bank of Canada’s preferred measures of core inflation showed further progress in March. The average of the three-month annualized rates of the Bank of Canada’s core-median and trim indicators slowed to just 1.3% (Graph 2) and the average of the year-over-year rates is down a tick to 3.0%. The Bank of Canada’s former favourite, CPIX, is also now up just 2.1% over the past year. Separately, the share of components in the CPI basket that are rising more than 3%, an indicator closely watched by Governor Macklem, is down to 38% from 41%. And the share of components showing price growth of less than 1% is up to 44% from 38% in February. Both suggest that the breadth of inflationary pressures is becoming more consistent with the Bank of Canada’s 2% target.

The inflation data for March should give monetary policymakers confidence that the progress made in taming consumer price pressures is sustainable. When Macklem said he wanted to see more of what he had seen in January and February, this type of release is what he was looking for. As a result, we are retaining our call for a rate cut in June. That said, cooperation from the federal government this afternoon and the next CPI release will both be key in seeing that forecast materialize.