- Florence Jean-Jacobs

Principal Economist

Economic News

Business Investment Bounces Back despite Still‑Declining Profits in Q1

May 31, 2024

Highlights

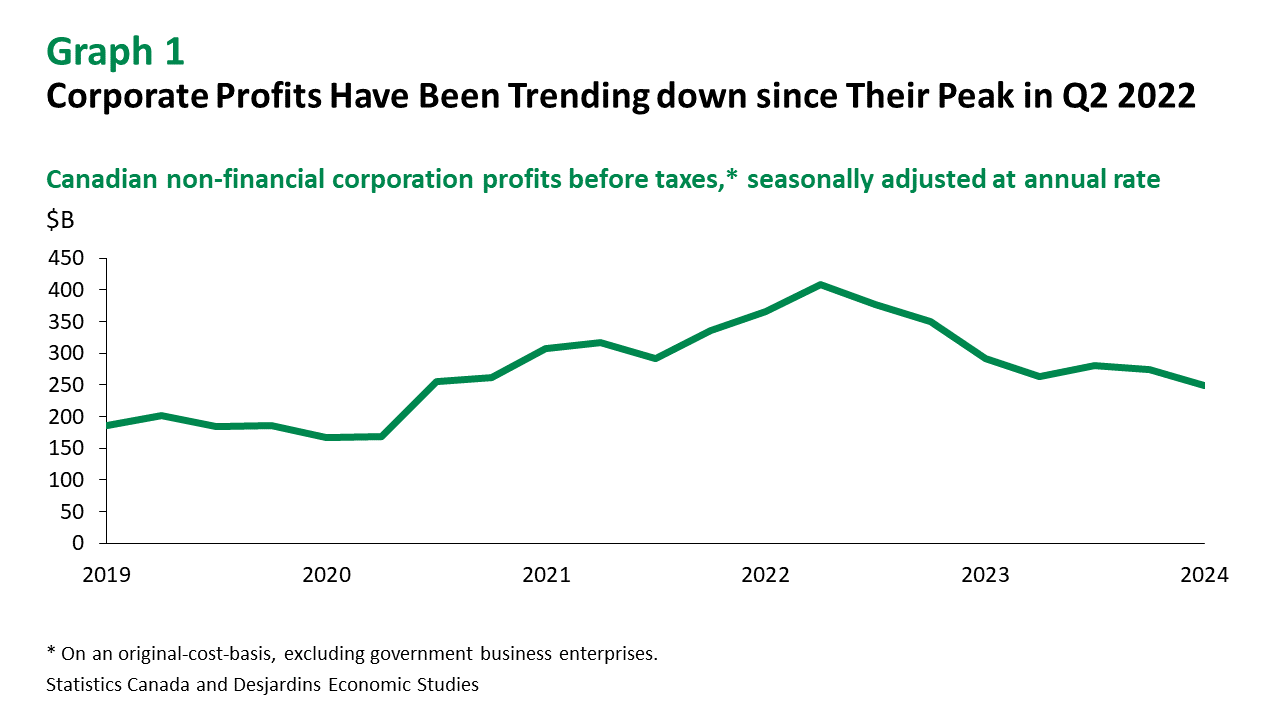

- Profits of Canadian non-financial corporations registered a substantial drop of 31.8% (q/q, annualized) in Q1 2024. With downward data revisions to previous quarters, this constitutes the sixth decline in the last seven quarters. Profits before tax (on an original-cost-basis) are down sharply from a year ago (14.5%), and now stand 39.1% below their Q2 2022 peak (graph 1).

- The wholesale industry, particularly farm product merchants, contributed most to the decline in net income before tax (NIBT) among non-financial corporations, driven by lower sales. The second-largest decline came from petroleum and coal products manufacturing due to declining revenues, which were primarily driven by lower prices. Motor vehicle and trailer manufacturing helped offset the declines in NIBT thanks to lower operating costs, bouncing back from net losses in the previous quarter.

- Meanwhile, non-residential business investment rebounded in Q1 after disappointing results at the end of last year. Both real and nominal investments rose, up 3.5% and 4.3% respectively, on a quarterly annualized basis (table 1). Firms in the oil and gas sector in particular upped their investments in engineering structures. Most investment categories registered increases, except for non-residential buildings, trucks and buses, as well as aircraft. Encouragingly, spending on intellectual property products also rose.

Implications

The current downward trend in corporate profits is not entirely surprising given the modest pace of economic activity and lower oil prices weighing on Canada’s oil and gas extraction and petroleum manufacturing industries. Businesses remain cautious and wary of subdued demand External link., while higher interest rates and input costs from the last year are still boosting their expenses.

The bright spot in the release is certainly the bounceback in business investment in Q1, thanks to higher spending on engineering and machinery and equipment. Whether this will continue in the coming quarters will depend on companies’ risk appetite and optimism. For those that were cautiously waiting for the clouds to clear before making sizeable investments, the prospect of declining interest rates may well lead to a shift towards more confidence to invest in growth projects and endeavours on a long time-horizon. With businesses facing accelerated tech transformations as well as climate and energy transition imperatives, many may be feeling a sense of urgency to maintain their competitiveness sooner rather than later.

Putting a slight damper on headline data is per capita real business investment, which remains at much lower levels than before the pandemic and is stalling. It at least halted its descent in Q1 (graph 2). Turning this slump around won’t be easy, but it’s an essential step towards addressing Canada’s underperforming productivity External link..